|

|

发表于 23-2-2017 07:05 PM

|

显示全部楼层

发表于 23-2-2017 07:05 PM

|

显示全部楼层

本帖最后由 icy97 于 28-2-2017 06:16 AM 编辑

外汇赚益带动.益纳利次季净利增52%

http://www.sinchew.com.my/node/1617795/

(吉隆坡24日讯)外汇赚益贡献,带动益纳利美昌(INARI,0166,主板科技组)截至2016年12月31日止第二季净利增长52.20%至6304万7000令吉,推动上半年净利走扬27.74%至1亿1105万1000令吉。

半年净利扬28%

第二季营业额下滑6.33%至2亿7505万1000令吉,导致上半年营业额走低2.10%至5亿5662万8000令吉。

派息1.8仙

同时管理层也宣布每股派息1.8仙。

展望截至2017年6月30日止财政年,该公司对无线电频及光学电子制造业务保持正面表现持谨慎乐观看法,同时也将持续从事新制造计划及寻找投资机会强化整体成长。

文章来源:

星洲日报/财经‧2017.02.24

SUMMARY OF KEY FINANCIAL INFORMATION

31 Dec 2016 |

| | INDIVIDUAL PERIOD | CUMULATIVE PERIOD | CURRENT YEAR QUARTER | PRECEDING YEAR

CORRESPONDING

QUARTER | CURRENT YEAR TO DATE | PRECEDING YEAR

CORRESPONDING

PERIOD | 31 Dec 2016 | 31 Dec 2015 | 31 Dec 2016 | 31 Dec 2015 | $$'000 | $$'000 | $$'000 | $$'000 |

| 1 | Revenue | 275,051 | 293,640 | 556,628 | 568,589 | | 2 | Profit/(loss) before tax | 64,363 | 44,838 | 114,328 | 88,774 | | 3 | Profit/(loss) for the period | 62,354 | 42,845 | 110,506 | 85,334 | | 4 | Profit/(loss) attributable to ordinary equity holders of the parent | 63,047 | 41,425 | 111,051 | 86,934 | | 5 | Basic earnings/(loss) per share (Subunit) | 6.54 | 4.45 | 11.56 | 9.41 | | 6 | Proposed/Declared dividend per share (Subunit) | 1.80 | 2.40 | 4.80 | 5.20 |

|

| AS AT END OF CURRENT QUARTER | AS AT PRECEDING FINANCIAL YEAR END | 7

| Net assets per share attributable to ordinary equity holders of the parent ($$) | 0.8242 | 0.7152

|

|

|

|

|

|

|

|

|

|

|

|

|

发表于 23-2-2017 07:06 PM

|

显示全部楼层

本帖最后由 icy97 于 24-2-2017 01:40 AM 编辑

益纳利在五年内飙升超过1000%

刘豪正刘豪正 2017年 02月 16日

http://cj.sharesinv.com/20170216/43955/

远古以来,历史告诉我们,科技是推动人类文明昌盛的动力;而在现今世代,半导体可能是成就手机及数码科技的工具。无可疑问,投资于半导体公司对寻求资本增长或价值的投资者而言,都应该是明智之举。

在长堤对岸,于大马交易所主板上市的益纳利(Inari Amertron)就是一家为半导体产品提供一系列制造服务的公司。具体来说,公司主要是为手机无线射频提供电子制造服务(EMS)及从事光电制造(optoelectronics manufacturing)。简而言之,公司为后端半导体包装提供一个组装平台,后者主要包含了后端晶片处理、组件组装及无线射频最后测试服务。

自从2011年7月首次公开售股(IPO)后,益纳利的股价升高了1016.7%至2017年2月8日的每股1.83令吉。我们可能没有注意到益纳利的壮观升势,不过,我们将为大家详细分析,看看其目前股价是否有进一步的上涨空间。

行业看涨及市场定位

我们在日常生活中肯定可以感受到手机及数据科技的日益增长。众所周知,这个冲击可能会继续扩大。从宏观的角度来看,对益纳利来说自然是一件好事,因为它可从中捕捉更大的商机。

《2016全球电子制造服务市场报告》指出,2015年电子组装市场的总值达到1万3,000亿美元,而这个市值预期至2020年增长至1万6,000亿美元,部分原因是受到对EMS的需求推动。次组装EMS的价值也相应地预期在同一期间以6.2%年复合增长率(CAGR)增长,从4,300亿美元增加至5,800亿美元。

基于益纳利最新的FY16全年业绩,其取得的收入相等于2亿5,910万美元,而其中的2亿4,400万美元是来自EMS业务。相比《2016全球电子制造服务市场报告》的估计,单单益纳利的EMS业务便占了全球在2016年对EMS需求的大约5.3%!

虽然这只是一个简单的推断,但我们可以得出的结论是益纳利所占的市场份额相当不错。同时,益纳利在FY16取得的6.4%收入增长也超越了对全球EMS价值的6.2% CAGR预估(从2015年至2020年)。

这进一步显示,益纳利的市场份额将会增加。值得一提的是,世界最大的半导体公司之一Broadcom (市值大约为810亿美元)是益纳利的长期大客户。

受惠于强劲美元

虽然益纳利是以马来西亚令吉运转,但公司保持一个以美元为主的外国银行户口,以方便存款及以美元为主的收入及采购,这为公司在外汇波动时,提供一个自然对冲机制。

与此同时,益纳利的大部分销售是以美元计价,但只有50%开支是以美元计算。这让益纳利可从美元兑令吉升值时受惠。基于对益纳利的敏感分析,令吉兑美元在FY16末每下跌1%,公司的净利将可增加120万令吉。

展望未来,随着美国联储局对加息持相对强硬态度,那么我们或许可以推测令吉兑美元将保持在低位或甚至进一步退跌,这对益纳利来说当然有利。

财务表现稳健

自2011年上市以来,益纳利的营业额以49.4%年复合增长率增长,从1亿4,020万令吉跳升至FY16的10亿令吉。毛利及净利也双双上涨,在同一期间每年分别以平均123.3%及99.6%增长。

与此同时,公司的债务也大幅减少。益纳利的债务在FY15达到最高的1亿零770万令吉,但在最新出炉的1Q17季度报告中,债务已减低至5,450万令吉。相应地,公司最新的资产负债表显示,总债务与股本比只得7.6%。

现金流方面,从营运而来的现金一直处于正数及在增长中,并从FY11的2,090万令吉以可观的52.2%年复合增长率增加至FY16的1亿7,040万令吉。因此,公司持有的现金从FY11的2,260万令吉增加至FY16的2亿1,240万令吉。

此外,最新的1Q17业绩也比去年同期出色。收入提高2.4%至2亿8,160万令吉;净利则增加5.5%至4,800万令吉。加上来自营运的另一笔8,260万令吉现金,公司持有的现金累积至2亿8,690万令吉。

由于持有大笔现金,益纳利的资产负债表流动性很高,流动比率为3.1倍,而公司产生现金的能力也让其可以更容易为自身的资本开支融资。同时,在最新的季度里,公司也处于净现金状态,总债务为2亿4,610万令吉。

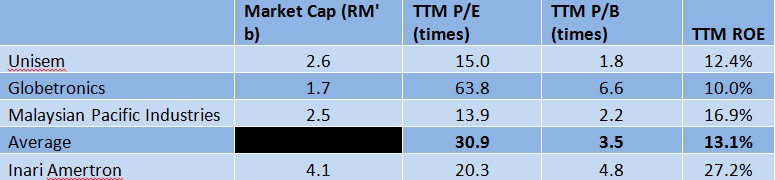

估值与同行相比

基于每股1.83令吉,益纳利是以大约过去12个月(TTM)的24.1倍本益比在交易。

相比之下,益纳利在马来西亚上市的同行是以11.2倍至35.2倍TTM本益比在交易,平均大约是19.1倍。益纳利似乎是以较高估值在交易。

不过,投资者也必须注意,益纳利的TTM股本回报率(ROE)为23.1%,比同行平均的14.1% 差不多翻了一倍,因此投资者不应马上认为益纳利目前的估值过高,而其股价的表现在很大程度上是合理的。

尽管我们认为益纳利是一家不折不扣的优质公司,但市场似乎已经给予益纳利合理估值。市场给予益纳利的目标价平均为每股1.87令吉,因此如果投资者目前进场似乎有点风险,而其潜在涨升空间只得2.2%。然而,投资者或许可以对益纳利的股价多加留意,在适当时机进场。 |

|

|

|

|

|

|

|

|

|

|

|

发表于 23-2-2017 07:06 PM

|

显示全部楼层

本帖最后由 icy97 于 24-2-2017 02:08 AM 编辑

EX-date | 15 Mar 2017 | Entitlement date | 17 Mar 2017 | Entitlement time | 04:00 PM | Entitlement subject | Second interim dividend | Entitlement description | Second interim single tier dividend of 1.8 sen per ordinary share in respect of the financial year ending 30 June 2017 | Period of interest payment | to | Financial Year End | 30 Jun 2017 | Share transfer book & register of members will be | to closed from (both dates inclusive) for the purpose of determining the entitlement | Registrar or Service Provider name, address, telephone no | MEGAPOLITAN MANAGEMENT SERVICES SDN BHDNo. 45-5, The BoulevardMid Valley CityLingkaran Syed Putra59200 Kuala LumpurTel: 03-2284 8311Fax: 03-2282 4688 | Payment date | 06 Apr 2017 | a.Securities transferred into the Depositor's Securities Account before 4:00 pm in respect of transfers | 17 Mar 2017 | b.Securities deposited into the Depositor's Securities Account before 12:30 pm in respect of securities exempted from mandatory deposit |

| | c. Securities bought on the Exchange on a cum entitlement basis according to the Rules of the Exchange. | Number of new shares/securities issued (units) (If applicable) |

| | Entitlement indicator | Currency | Currency | Malaysian Ringgit (MYR) | Entitlement in Currency | 0.018 | Par Value | Malaysian Ringgit (MYR) 0.000 |

|

|

|

|

|

|

|

|

|

|

|

|

发表于 8-3-2017 01:01 AM

|

显示全部楼层

发表于 8-3-2017 01:01 AM

|

显示全部楼层

本帖最后由 icy97 于 10-3-2017 02:46 AM 编辑

icy97 发表于 9-3-2016 03:14 AM

益納利美昌斥4450萬 購PCL科技9.7%股權

2016年3月08日

(吉隆坡8日訊)益納利美昌(INARI,0166,主要板科技)以3.55億台幣(約4450萬令吉)收購PCL科技公司9.7%股權,同時雙方在中國成立聯營公司提供外包半導 ...

益纳利美昌终止与众达联营

2017年3月3日

(吉隆坡2日讯)几经讨论后,益纳利美昌(INARI,0166,主板科技股)与众达科技有限公司(PCL Technologies)决定终止早前所签署的了解备忘录,探讨联营一事也将停止。

益纳利美昌向马交所报备,由于双方无法成立一个符合两者业务策略的联营公司,经过数个月的努力和讨论后,双方决定终止该备忘录。

因此,探讨成立联营一事也将随之停止。

益纳利美昌表示,这不会显著影响公司财务,而公司也将持续在中国探索其他有助于扩大旗下外包半导体封装和测试(OSAT)业务的潜在商机。

去年3月8日,益纳利美昌以3亿5500万新台币(约4450万令吉),收购众达科技的9.7%股权,同时探讨和后者成立联营公司。

当时,双方有共同的目标和意愿,在5年内把联营公司在中国交易所挂牌。 【e南洋】

Type | Announcement | Subject | OTHERS | Description | INARI AMERTRON BERHAD ("INARI" OR "THE COMPANY")- MEMORANDUM OF UNDERSTANDING ("MOU") BETWEEN INARI AND PCL TECHNOLOGIES INC ("PCL") | Reference is made to the announcements made by the Company on 8 March 2016, 6 May 2016, 1 July 2016 and 4 November 2016 in relation to the MOU between Inari and PCL on the intention to set up a joint-venture entity (“JVE”) in the People’s Republic of China (“PRC”) for purposes of providing outsourced semiconductor assembly and test (“OSAT”) services to major customers in PRC, with particular focus on front-end OSAT services.

The Board wishes to announce that after various efforts and numerous discussions between Inari and PCL during the past months, both parties were not able to form the JVE with a configuration that could satisfy the business strategies of both parties to meet the objectives stated in the MOU. Thus, Inari and PCL have decided jointly and mutually to terminate the MOU and hence negotiations with respect to the formation of the JVE have ceased. This termination does not have any financial impact on the Company.

Notwithstanding the termination, the Company will continue to explore other potential business opportunities in the PRC that will be useful for the expansion of the Company’s OSAT business.

This announcement is dated 2 March 2017. |

|

|

|

|

|

|

|

|

|

|

|

|

发表于 10-3-2017 03:51 AM

|

显示全部楼层

益纳利美昌

中止联营影响不大

2017年3月4日

分析:大马投行

目标价:2.15令吉

最新进展:

益纳利美昌(INARI,0166,主板科技股)与众达科技有限公司(PCL Technologies)终止解备忘录,停止探讨联营。

原因是双方无法达成协议,设立一家符合两者业务策略的联营公司。

但益纳利美昌将继续在中国,探索其他有助扩大外包半导体封装和测试(OSAT)业务的商机。

行家建议:

管理层指出,停止合作原因是双方手上持有优先项目,如益纳利美昌的虹膜扫描零件新生产线。

在中国发展OSAT业务喊停,但若未来时机成熟,不排除与PCL重新合作。

另一方面,通过中国子公司Amerton Technology Kunshan公司(简称ATK),可让益纳利美昌抓住当地半导体行业的增长。

我们预测,ATK在2016财年共占营业额约10%。

尽管错失扩展OSAT业务机会,但对益纳利美昌的虹膜扫描科技业务持乐观。

维持“守住”评级,目标价2.15令吉。

【e南洋】 |

|

|

|

|

|

|

|

|

|

|

|

发表于 15-3-2017 08:05 PM

|

显示全部楼层

本帖最后由 icy97 于 16-3-2017 01:12 AM 编辑

【寿司皇者】- INARI (0166) 业绩突破新高,BROADCOM引领涨潮!

Wednesday, March 15, 2017

http://harryteo.blogspot.my/2017/03/1393-inari-0166-broadcom.html

INARI(0166)是大马科技板块市值最大的科技股,市值 = RM3,766 Mil. 股价在3月8号突破历史新高RM1.99(今年1送1红股),一度上涨到RM2.01。这个星期股价下滑了2-3%,加上今天1.8分的股息刚刚除权,因此股价调整到RM1.91。

市值排名前5的分别是: 1.INARI 2.UNISEM 3.MPI 4.GTRONIC 5.JCY

而股价涨幅排名如下: - 以下是3月15日12.30休市的价格 1.MPI,RM10.14, +36.84% 2.GTRONIC, RM4.74, +36.21% 3.JCY, RM0.655, +33.67% 4.UNISEM, RM3.00, + 27.12% 5. INARI, RM1.91, + 15.06%

5家公司的股价平均在2017年上涨了29.78%,UNISEM以及GTRONIC的盈利在最新季度有所下滑,其余3家都获得了质的飞跃。MPI以及INARI的盈利都突破历史新高,而JCY也由亏转盈。今天想要跟大家聊到的就是外号【寿司】的INARI,大家一起研究这家公司近年的发展。

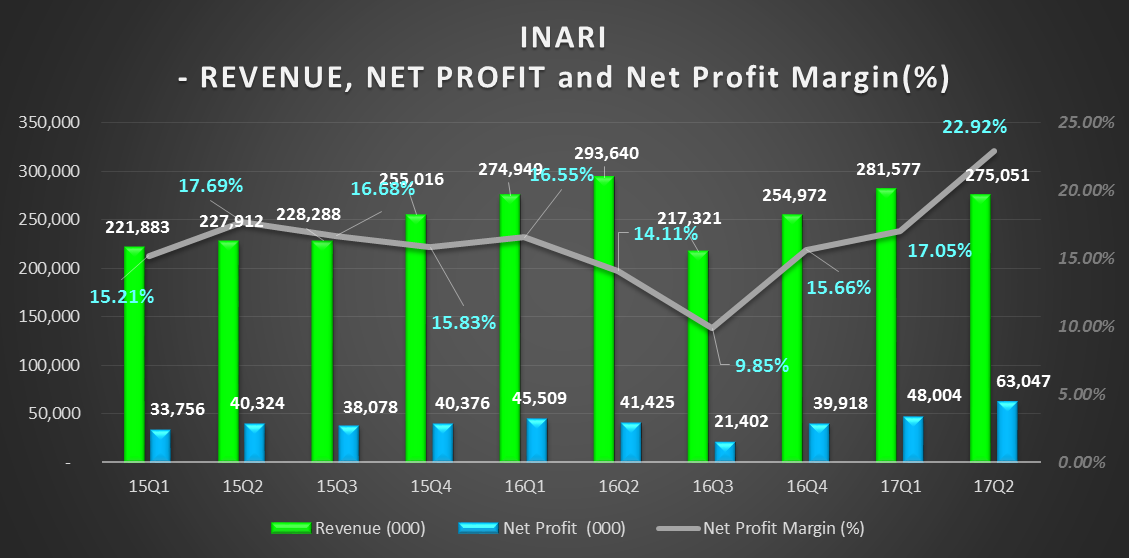

INARI (0116) 最新季度的盈利突破了历史新高,但是营业额却比上个季度下滑了RM6 mil。这主要是因为有有RM23.1 mil的外汇盈利以及RM5.596 mil的Grant Income,Gross Profit = RM56.643mil比去年的RM63.306 mil低了10.5%。

不过之前美金走低的时候,公司也面临了外汇亏损。所以现在美金处于高位,INARI有外汇盈利是必然的。而且16Q3的业绩以及盈利是11个季度里最低的,其中一个原因是因为美金下滑。因此未来两个季度(17Q3 & Q4)要保持YOY成长应该不成问题:

这个季度(1月 – 3月)跟去年同期的差别是:

- 现在的USD/MYR平均是4.45 , 而之前是4.22, 相差了5%

- 新厂已经完工,预计FY17开始贡献盈利

- 2016年全年半导体成长只有1.1%,但是2017年预计会有3.3%

- 科技领域+美金股是近期的趋势,INARI会有趋势护航

- Net Cash Positon = RM299 mil比去年同期进步

- 全球1月半导体销售非常亮眼,预计大马半导体科技股也会获益

- APPLE预计在今年Q3会出新的IPHONE, Broadcom的订单预计会走高,间接会刺激INARI的销售。

此外,电子电器产品出口按年增加11.4%, 整体1月出口按年增加了13.6%,是历史上最佳的1月记录。全球的制造业复苏将会带动大马的出口强劲成长,而且中国以及美国对大马的电子产品需求有所上升。因此预计INARI这个季度的盈利不会突破历史新高,但是要保持正面的成长是不难的。

不过需要注意的是,下半年或许会放缓,原因是特朗普有可能会实施保护主义,这将会影响大马出口表现。而且大型商品的价格不断攀升,这也将会增加制造业务的成本。

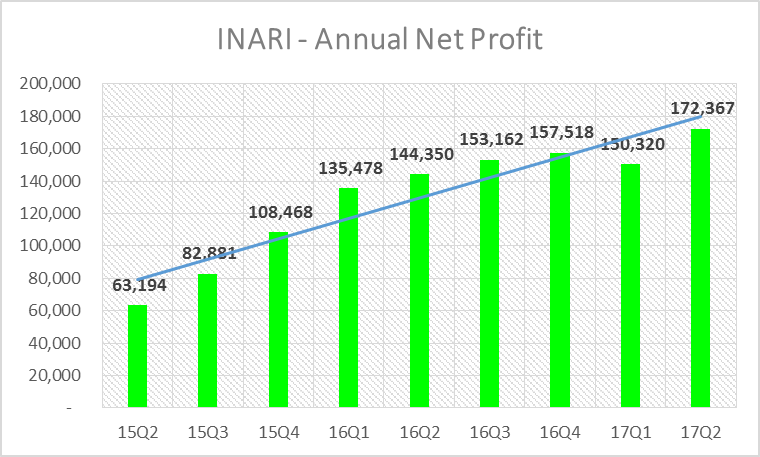

INARI的全年盈利在这个季度突破历史新高,来到了RM172.367 mil,因此股价在3月2日突破历史新高的RM1.98, 股价一度触碰到RM2.00.

3月2日的成交量27.2 mil股,这个成交量是3个月新高。

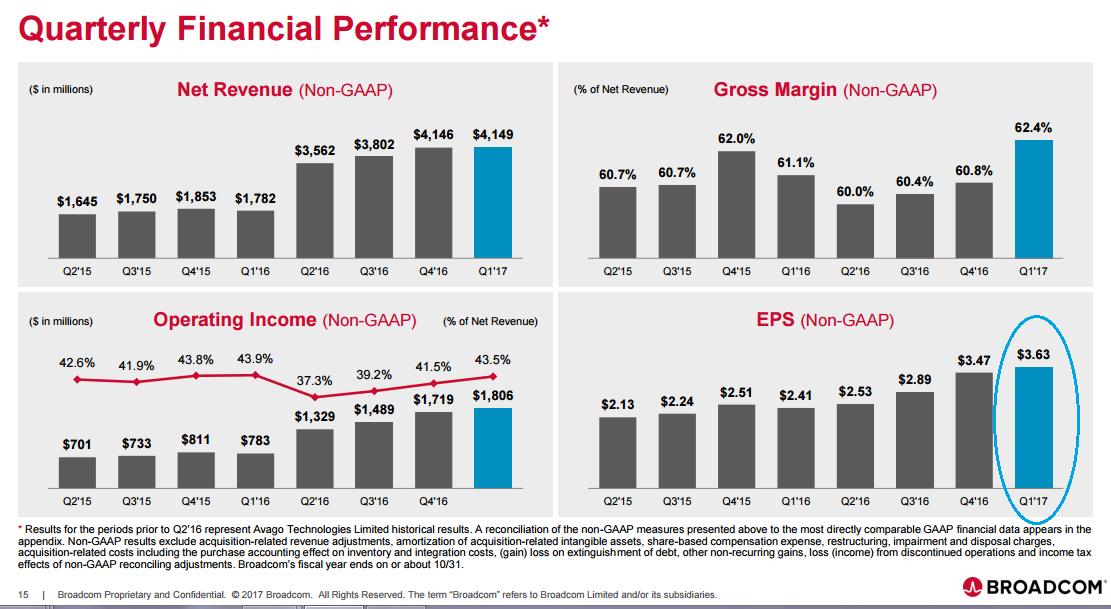

什么原因导致INARI的股价破新高,上图相信可以为大家解惑。INARI最大的客户是BROADCOM ,因此3月1号BROADCOM公布了新高的盈利, EPS = US3.63。有关注BROADCOM的业绩报告的投资者自然会因为这个好消息而买进INARI.

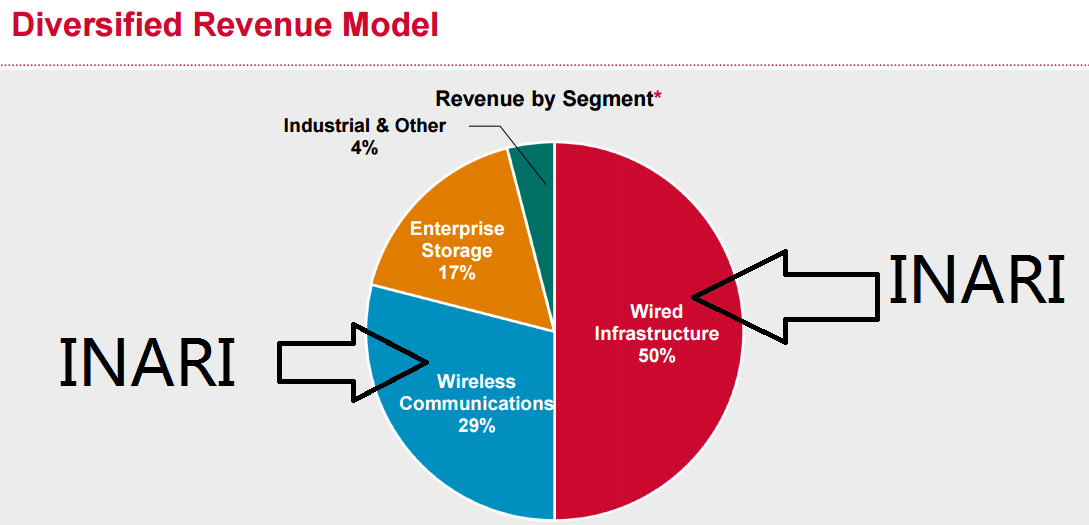

以上是BROADCOM的业务分布图,其中79%是来自Wireless Communications 以及Wired Infrastructure。而BROADCOM主要是负责设计产品,Production都outsource出去。INARI就是负责这两个部分的production,理论上BROADCOM的业绩好,INARI的赢也会好。BROADCOM这次的季度是16年11月 – 17年1月,结合【大马电子出口数据】+【Broadcom】的数据,我们可以预测到1月份INARI的销售应该很不错。至于2 - 3月份的业绩就要看美金的走势以及大马的出口数据。

INARI的业务80%来自BROADCOM, 很多人都担心假设BROADCOM不跟INARI合作,INARI要怎么办。BROADCOM的CEO是一位华人,而且还是PENANG人。根据槟城科技业的朋友说,INARI的管理层和这位BROADCOM的CEO已经认识以及合作多年,因此短期内应该不会结束合作关系。

总结:

INARI现在的PE = 21.85,科技股的PE 大多是15 - 25之间,而INARI过往今年的PE 介于20 - 25。所以以现在的估值来看,INARI是处于偏高水平。不过16Q3以及Q4的盈利都4个季度的最差的两个季度,美金走高以及半导体销售增长的情况下,INARI未来2 - 3个季度的盈利成长将会非常诱人。

根据最新的投行分析,CIMB分别给予INARI高达RM2.20的Target Price,而MPI的Target Price则是RM11.00。INARI预计会在17年3月把他们的RF Tester从700架增加到780架以满足他们主要客户的需求。此外,新的部门“INARI OPTICAL TECHNOLOGY"将会注重在Iris Scanners的研发。投行也非常看好这个业务,预计未来会为公司带来新的盈利贡献。

MMSV告诉媒体,它们的订单会因为APPLE发布新机款而走高,预计FY2017会优于FY2016.因此身为龙头老大的INARI应该也会分到一块肉吃,加上新厂已经开始贡献盈利,预计FY17会再创新的里程碑。

|

|

|

|

|

|

|

|

|

|

|

|

发表于 16-5-2017 06:16 PM

|

显示全部楼层

本帖最后由 icy97 于 23-5-2017 06:44 AM 编辑

益纳利美昌第三季净利大涨近140%

Wong Ee Lin/theedgemarkets.com

May 16, 2017 20:30 pm MYT

http://www.theedgemarkets.com/article/益纳利美昌第三季净利大涨近140

(吉隆坡16日讯)益纳利美昌(Inari Amertron Bhd)2017财政年第三季(截至2017年3月31日止)的净利大涨139.13%至5118万令吉,上财年同季仅净赚2140万令吉。

当季的每股净利也从上财年同季的1.11仙,跳涨至2.62仙。

该集团今日通过大马交易所发文告报备,第三季净利扩增主要是产品需求走高,以及产品结构变动所致。

营业额也按年增长26.1%至2亿7403万令吉,上财年同季录得2亿1732万令吉。

益纳利美昌也宣布,2017财年派发每股2.2仙的第三次单层中期股息,派息日落在7月6日。

综合2017财年首9个月的业绩表现,该集团净赚1亿6223万令吉,或每股8.37仙,同期净利累积至1亿834万令吉,或每股5.69仙,涨幅高达49.75%。

合共3季营业额按年走高5.69%至8亿3066万令吉,同期则为7亿8591万令吉。

瞻望未来,基于无线射频和光电产品业务的制造活动持续进行,益纳利美昌仍审慎乐观看待2017财年或录得正面的业绩表现。

“我们在本财年稍早也投资一个新虹膜扫描制造项目,该项目在本季度开始为集团营业额带来进账。本集团也将继续进行新制造项目,以提高整体的业绩增长。”

(编译:倪嫣鴽)

SUMMARY OF KEY FINANCIAL INFORMATION

31 Mar 2017 |

| | INDIVIDUAL PERIOD | CUMULATIVE PERIOD | CURRENT YEAR QUARTER | PRECEDING YEAR

CORRESPONDING

QUARTER | CURRENT YEAR TO DATE | PRECEDING YEAR

CORRESPONDING

PERIOD | 31 Mar 2017 | 31 Mar 2016 | 31 Mar 2017 | 31 Mar 2016 | $$'000 | $$'000 | $$'000 | $$'000 |

| 1 | Revenue | 274,033 | 217,321 | 830,661 | 785,910 | | 2 | Profit/(loss) before tax | 54,277 | 23,031 | 168,605 | 111,805 | | 3 | Profit/(loss) for the period | 52,162 | 22,743 | 162,668 | 108,077 | | 4 | Profit/(loss) attributable to ordinary equity holders of the parent | 51,178 | 21,402 | 162,229 | 108,336 | | 5 | Basic earnings/(loss) per share (Subunit) | 2.62 | 1.11 | 8.37 | 5.69 | | 6 | Proposed/Declared dividend per share (Subunit) | 2.20 | 1.00 | 7.00 | 6.20 |

|

| AS AT END OF CURRENT QUARTER | AS AT PRECEDING FINANCIAL YEAR END | 7

| Net assets per share attributable to ordinary equity holders of the parent ($$) | 0.4252 | 0.7152

|

|

|

|

|

|

|

|

|

|

|

|

|

发表于 17-5-2017 01:17 AM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 17-5-2017 06:09 AM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 17-5-2017 09:36 AM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 19-5-2017 03:24 AM

|

显示全部楼层

EX-date | 06 Jun 2017 | Entitlement date | 08 Jun 2017 | Entitlement time | 04:00 PM | Entitlement subject | Interim Dividend | Entitlement description | Third interim single tier dividend of 2.2 sen per ordinary share in respect of the financial year ending 30 June 2017 | Period of interest payment | to | Financial Year End | 30 Jun 2017 | Share transfer book & register of members will be | to closed from (both dates inclusive) for the purpose of determining the entitlement | Registrar or Service Provider name, address, telephone no | MEGAPOLITAN MANAGEMENT SERVICES SDN BHDNo. 45-5, The BoulevardMid Valley CityLingkaran Syed Putra59200 Kuala LumpurTel : 03-2284 8311Fax : 03-2282 4688 | Payment date | 06 Jul 2017 | a.Securities transferred into the Depositor's Securities Account before 4:00 pm in respect of transfers | 08 Jun 2017 | b.Securities deposited into the Depositor's Securities Account before 12:30 pm in respect of securities exempted from mandatory deposit |

| | c. Securities bought on the Exchange on a cum entitlement basis according to the Rules of the Exchange. | Number of new shares/securities issued (units) (If applicable) |

| | Entitlement indicator | Currency | Currency | Malaysian Ringgit (MYR) | Entitlement in Currency | 0.022 | Par Value (if applicable) | Malaysian Ringgit (MYR) 0.000 |

|

|

|

|

|

|

|

|

|

|

|

|

发表于 21-5-2017 05:27 PM

|

显示全部楼层

本帖最后由 icy97 于 23-5-2017 03:22 AM 编辑

益纳利美昌

赚幅推高财测

2017年5月18日

分析:艾芬黄氏投资

目标价:2.60令吉

最新进展:

益纳利美昌(INARI,0166,主板科技股)截至3月31日第三季,净利按年上扬1.39倍,并派息每股2.2仙。

第三季净利为5117万8000令吉,或每股2.62仙,优于上财年同期的2140万2000令吉,或每股1.11仙。

第三季营业额也按年增加26.10%,至2亿7403万3000令吉,上财年同期则录得2亿1732万1000令吉。

累计首9个月,净利按年上扬49.75%,至1亿6222万9000令吉;营业额年增5.69%,至8亿3066万1000令吉。

行家建议:

益纳利美昌2017财年首9个月,核心净利按年上涨22%,达1亿3500万令吉;超越我们的预期,不过符合市场预期,分别占全年预测的84%及70%。

该公司的核心净利表现超越我们的预期,是因为当季的扣除利息、税务、折旧与摊销前盈利(EBITDA)赚幅,按季增加6个百分点至26.1%。

该公司首9个月的EBITDA赚幅,企于22.1%,超越我们2017财年预测的19.7%。

纳入更高的赚幅后,我们也上调2017财年的每股净利预测,涨幅为11%。不过,维持2018至2019财年的每股净利预测。

【e南洋】

虹膜扫描模块成推手.益纳利美昌财测不变

(吉隆坡17日讯)益纳利美昌(INARI,0166,主板科技组)2017财政年9个月财报符合预期,分析员认为射频业务将受技术过度影响,但新虹膜扫描模块业务可能成为新营收推手,普遍维持财测不变。

益纳利美昌2017财政年首9个月核心净利1亿5260万令吉符合预期,兴业研究认为,射频(RF)环节可能在今年或明年初达到850个试验器,以满足客户今年6月至7月涌现的新订单。

但达证券说,受到晶圆尺寸从6吋转移至8吋影响,集团2017财政年射频业务营收料停滞不前。

不过,虹膜扫描模块业务有望成为新业务亮点,大马投行说,益纳利美昌近期入袋的虹膜扫描模块合约将推动2018财政年营业额增长18%。

目前,益纳利美昌已投资2500万令吉来筑起每月500万单位产能,并放眼2018财政年再投放7500万令吉进一步扩充产能,兴业研究预见集团2019年每月产量将达到2000万至2500万单位。

股价潜在涨势受限

整体来看,各大证券行普遍维持益纳利美昌财测和投资评级不变,但MIDF研究说,尽管益纳利美昌前景不俗,但股价今年来已上扬32.5%,相信股价潜在涨势已经受限,因此下调投资评级。

“不过,该股周息率达到诱人的5%水平,仍是拥抱股息投资策略的投资者良好的投资选项。”

文章来源:

星洲日报‧财经‧报道:洪建文‧2017.05.17 |

|

|

|

|

|

|

|

|

|

|

|

发表于 18-6-2017 02:08 PM

|

显示全部楼层

本帖最后由 icy97 于 18-6-2017 04:38 PM 编辑

INARI AMERTRON – POISED FOR A TECH SUPERCYCLE?

Don Low June 16, 2017

http://aspire.sharesinv.com/48264/don-low-inari-amertron-poised-for-a-tech-supercycle/

Tech heavy Nasdaq Composite took a beating last Friday when Goldman Sachs and UBS suggested that tech stocks are potentially overheated.

The scepter of a bubble being suggested also sparked a comparison of valuation between today’s soaring tech stocks versus that in 1999’s dot-com bubble. But the case is different this time round, the top tech stocks today – also known as – FAAMG (Facebook, Apple, Amazon, Microsoft and Google) are dowdy monopolies generating vast amount of positive free cash flow while their revenue and earnings grow at double digits.

That said, stocks in Nasdaq are not exactly going cheap, so we looked to Malaysia-listed Inari Amertron again.

Investment Moats

In the past five years, shares of Inari Amertron have surged multi-folds from RM0.09 to RM2.05 today, after adjusting for stock splits. The jump represents a 2277.8 percent increase in stock price!

We only identified Inari Amertron in February 2017 when the shares were trading at about RM1.83. Although the consensus target price back then was RM1.87, its shares have rallied further by another 12 percent to today’s RM2.05.

In our last article, Shares Investment estimated that Inari Amertron has a strong market position in the Electronic Manufacturing Services (EMS) industry, commanding about 5.3 percent of global market share in 2016. The EMS industry was estimated to be a US$430 billion industry in 2015 and expected to grow to US$580 billion by 2020 – approximately at a compounded annual growth rate of 6.2 percent. In addition, growing radio frequency content growth per smartphone is also one of Inari Amertron’s potential growth driver.

Latest Financial Results

In its latest financial result, 9M17, Inari Amertron generated revenue of RM830.7 million surpassing that of the previous year by 5.7 percent on higher demand for the company’s products. The bottom line was further lifted by higher other operating income of RM44.8 million (9M16: RM10.9 million). Correspondingly, Inari Amertron’s net profit grew 49.7 percent higher over the past year to RM162.2 million.

On the cash flow front, Inari Amertron managed to produce higher free cash flow of RM128.2 million compared to RM6.2 million in 9M16. This was despite the fact that cash spent on capital expenditure was about the same at RM70.4 million.

The net cash inflow for the period further strengthened the company’s financial position. Inari Amertron’s cash position rose from RM248.8 million in 9M16 to RM380.9 million as at the end of 9M17. Meanwhile, total debt was pared down from RM80.4 million to RM48.4 million, as the company improved its total debt-to-equity ratio from 12.4 percent to 5.8 percent. Concurrently, Inari Amertron’s net cash position was also boosted from RM168.4 million in 9M16 to RM332.5 million in 9M17.

Undemanding Valuation

At the share price of RM2.05, Inari Amertron is changing hands at about 20.3 times price-to-earnings (P/E), lower than its peers average of 30.9 times. The counter is also trading at a lower P/E than the 24.1 times in February, while at the same time, return-on-common equity improved from 23.1 percent to 27.2 percent.

We look to another financial metric to determine if Inari Amertron is indeed undervalued. Earnings-per-share (EPS) grew from RM0.057 in 9M16 to RM0.084 in 9M17. Correspondingly, EPS growth for the past year was about 47.4 percent. At the current P/E of 20.3 times, Inari Amertron would register a price-to-earnings growth (PEG) of 0.43 times only.

As such, given its track record of earnings growth, robust balance sheet, and undemanding valuation we think Inari Amertron allows investors to tap on the potential tech supercycle. If not, we think this counter also provides a good margin of safety, in case the bubbling narrative comes true.

|

|

|

|

|

|

|

|

|

|

|

|

发表于 9-8-2017 06:16 AM

|

显示全部楼层

益纳利末季净利有望大增.推动全年创高峰

(吉隆坡8日讯)益纳利美昌(INARI,0166,主板科技组)盈利有望创下6连涨佳绩,马银行研究预期本月22日公布的第四季净利将大增至5700万至6300万令吉,全年财报将再创高峰,并看好在稳定射频(RF)需求,以及红外线LED需求增长下,2018财政年盈利增幅料可延续强势。

马银行研究相信3大高档智能手机将在第三季推介,有望拉高射频需求,进而扶持益纳利美昌盈利增长,预期集团本月公布的2017财政年第四季净利将按季增长22至34%,达到5700万至6300万令吉。

“此外,红外线LED也有望带来满季的盈利贡献,这有望为集团带来可观的获利表现。”

数据显示,全球半导体销售连续4个月走扬,6月销售按年增长24%至326亿美元,同时半导体设备商出货金额也年增33%,但后者增速略有减缓,主要是多数半导体领域资本开销已再今年上半年投放。

马银行研究认为,半导体领域资本开销投放将确保今年下半年半导体销售增长将更为强劲,也是投资者转向益纳利美昌等半导体公司的最佳时机。

“通过博通(Broadcom)大举曝险于利基射频领域,益纳利美昌盈利增长纪录无疑是大马半导体股最佳,同时随着5G网络的逐步采用,集团未来3年仍将提供卓越的盈利能见度。”

此外,益纳利美昌新投资的红外线LED业务,也有望成为未来的盈利推手,因此马银行研究维持“买进”评级,目标价从2令吉45仙调高至2令吉70仙。

文章来源:

星洲日报‧财经‧报道:洪建文‧2017.08.08 |

|

|

|

|

|

|

|

|

|

|

|

发表于 19-8-2017 04:08 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 22-8-2017 10:03 PM

|

显示全部楼层

本帖最后由 icy97 于 24-8-2017 04:49 PM 编辑

益纳利末季净利飙64%.派息2.8仙

http://www.sinchew.com.my/node/1675255/

(吉隆坡22日讯)归功于产品需求旺盛、脱售上市公司股权,益纳利美昌(INARI,0166,主板科技组)截至2017年6月30日第四季净利大起64.4%,从前期的3991万8000令吉增至6562万4000令吉,推动全年净利走扬53.69%,至2亿2785万3000令吉。

末季营业额上扬34.38%,至3亿4565万令吉,托高全年营业额12.77%,至11亿7631万1000令吉。

该公司董事部建议派发每股2.8仙(2.3仙中期+0.5仙特别)股息,除权和享有日落在9月18和20日。

益纳利美昌发文告表示,对截至2018年6月30日新财政年前景感到审慎乐观,主要是无线射频(RF)和光电,甚至是虹膜扫描产品制造业务有望持续跟随领域,乃至全球半导体市场增长。

“同时,集团继续落实新制造工程来提升整体涨势。”

文章来源:

星洲日报‧财经‧2017.08.23

| 0166 INARI INARI AMERTRON BERHAD | | Quarterly rpt on consolidated results for the financial period ended 30/06/2017 | | Quarter: | 4th Quarter | | Financial Year End: | 30/06/2017 | | Report Status: | Unaudited | | Submitted By: |

|

| | | Current Year Quarter | Preceding Year Corresponding Quarter | Current Year to Date | Preceding Year Corresponding Period | | | 30/06/2017 | 30/06/2016 | 30/06/2017 | 30/06/2016 | | | RM '000 | RM '000 | RM '000 | RM '000 | | 1 | Revenue | 345,650 | 257,210 | 1,176,311 | 1,043,120 | | 2 | Profit/Loss Before Tax | 72,223 | 41,326 | 240,828 | 153,131 | | 3 | Profit/(loss) attributable to ordinary equity holders of the parent | 65,624 | 39,918 | 227,853 | 148,254 | | 4 | Net Profit/Loss For The Period | 66,055 | 39,014 | 228,723 | 147,091 | | 5 | Basic Earnings/Loss Per Shares (sen) | 3.31 | 2.02 | 11.68 | 7.76 | | 6 | Dividend Per Share (sen) | 2.80 | 2.20 | 9.80 | 8.40 | | | | | As At End of Current Quarter | As At Preceding Financial Year End | | 7 | Net Assets Per Share (RM) | | | 0.4391 | 0.7152 |

|

|

|

|

|

|

|

|

|

|

|

|

|

发表于 22-8-2017 10:07 PM

|

显示全部楼层

自从2011年7月首次公开售股(IPO)后,益纳利的市值已破50亿大关!! |

|

|

|

|

|

|

|

|

|

|

|

发表于 22-8-2017 11:13 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 23-8-2017 03:38 AM

|

显示全部楼层

EX-date | 18 Sep 2017 | Entitlement date | 20 Sep 2017 | Entitlement time | 04:00 PM | Entitlement subject | Special Dividend | Entitlement description | Special single tier dividend of 0.50 sen per ordinary share | Period of interest payment | to | Financial Year End | 30 Jun 2017 | Share transfer book & register of members will be | to closed from (both dates inclusive) for the purpose of determining the entitlement | Registrar or Service Provider name, address, telephone no | MEGAPOLITAN MANAGEMENT SERVICES SDN BHDNo. 45-5, The BoulevardMid Valley CityLingkaran Syed Putra59200 Kuala LumpurTel: 03-2284 8311Fax: 03-2282 4688 | Payment date | 06 Oct 2017 | a.Securities transferred into the Depositor's Securities Account before 4:00 pm in respect of transfers | 20 Sep 2017 | b.Securities deposited into the Depositor's Securities Account before 12:30 pm in respect of securities exempted from mandatory deposit |

| | c. Securities bought on the Exchange on a cum entitlement basis according to the Rules of the Exchange. | Number of new shares/securities issued (units) (If applicable) |

| | Entitlement indicator | Currency | Currency | Malaysian Ringgit (MYR) | Entitlement in Currency | 0.005 |

|

|

|

|

|

|

|

|

|

|

|

|

发表于 23-8-2017 03:39 AM

|

显示全部楼层

EX-date | 18 Sep 2017 | Entitlement date | 20 Sep 2017 | Entitlement time | 04:00 PM | Entitlement subject | Interim Dividend | Entitlement description | Fourth interim single tier dividend of 2.3 sen per ordinary share | Period of interest payment | to | Financial Year End | 30 Jun 2017 | Share transfer book & register of members will be | to closed from (both dates inclusive) for the purpose of determining the entitlement | Registrar or Service Provider name, address, telephone no | MEGAPOLITAN MANAGEMENT SERVICES SDN BHDNo. 45-5, The BoulevardMid Valley CityLingkaran Syed Putra59200 Kuala LumpurTel: 03-2284 8311Fax: 03-2282 4688 | Payment date | 06 Oct 2017 | a.Securities transferred into the Depositor's Securities Account before 4:00 pm in respect of transfers | 20 Sep 2017 | b.Securities deposited into the Depositor's Securities Account before 12:30 pm in respect of securities exempted from mandatory deposit |

| | c. Securities bought on the Exchange on a cum entitlement basis according to the Rules of the Exchange. | Number of new shares/securities issued (units) (If applicable) |

| | Entitlement indicator | Currency | Currency | Malaysian Ringgit (MYR) | Entitlement in Currency | 0.023 |

|

|

|

|

|

|

|

|

|

|

| |

本周最热论坛帖子 本周最热论坛帖子

|

1579

1579  108

108