|

|

【SPH T39 交流专区】新加坡报业控股 SINGAPORE PRESS HLDGS LTD

[复制链接]

|

|

|

楼主 |

发表于 4-10-2007 11:14 PM

|

显示全部楼层

Incorporation of Subsidiary Company

Singapore Press Holdings Limited ("SPH") is pleased to announce that ithas today entered into a joint venture agreement with Fung ChoiPrinting Limited ("Fung Choi") and Rainbowchina Image Company Limited.SPH entered into the joint venture agreement through its wholly-ownedsubsidiary, SPH Interactive International Pte Ltd and 50% associatecompany, 701Search Pte Ltd.

The authorised and paid up capital of the joint venture company, whichis registered in Hong Kong and named 701Sou (Hong Kong) Pte Limited(701搜有限公司), will be SGD 25 million. The shareholding percentages willbe as follows:

SPH Interactive International 60%

Fung Choi Printing Limited 15%

Rainbowchina Image Company Limited 15%

701Search Pte Ltd 10%

The principal activity of this joint venture company is to providedigital media services in the PRC market, including the provision ofonline and mobile search services.

The joint venture transaction has no material financial impact on the results of SPH in the current financial year.

None of the directors of SPH have any interest, direct or indirect in this joint venture transaction.

|

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 14-10-2007 04:54 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 15-10-2007 09:23 AM

|

显示全部楼层

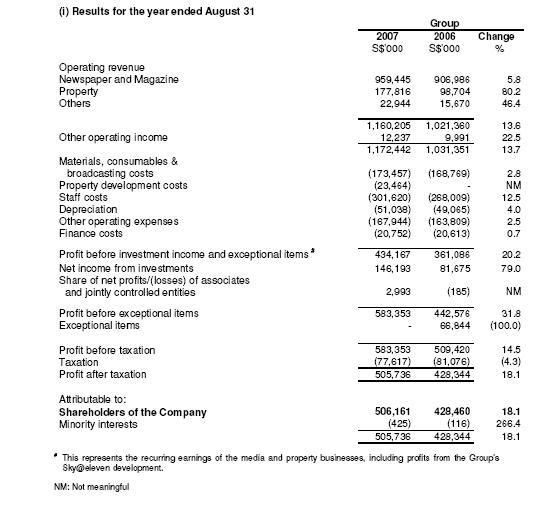

新報業控股截至8月底

全年淨利逾11億

(新加坡14日訊)新加坡報業控股截至今年8月底的財年全年淨利達5億620萬元(11億1364萬令吉),集團將在12月27日派發每股19分(42仙)的年終免稅股息。

報業控股主席陳慶炎博士昨天在業績發佈會上宣佈,和去年相比,今年報業控股的全年淨利上漲18.1%。

集團不包括投資收入和特殊賬項在內的全年營業盈利,則上升20.2%至4億3420萬元(9億5524萬令吉)。包括報業控股銷售在湯申路上段發展的共管公寓項目天一閣(Sky@Eleven),取得的4780萬元(1億零516萬令吉)初次盈利。

陳博士指出,集團將派發的每股19分年終免稅股息,是由每股9分的普通股息和每股10分的特別股息組成。加上早前已派發的中期股息,集團在2007財政年的總股息是26分。

陳博士透露,報業控股將繼續加強在報章領域的地位。

“我們目前正在整合晚報和新明的新聞室,晚報已經進行改革,並將在星期一推出。新明則將在稍后進行改革。”

此外,報業控股目前在本地和區域互聯網上投入的資金約5000萬元(1億1000萬令吉)。集團估計在接下來幾年,將至少投入另外5000萬元。

報業控股取得的各項佳績

★集團全年營業收入:增13.6%,達25億5200萬令吉

★報章與期刊業務:增5.8%,至9億5940萬元(21億1068萬令吉)

★平面廣告收入:增7.2%,至7億2510萬元(15億9522萬令吉)

★房地產收入:增80.2%,至1億7780萬元(3億9116萬令吉)(包括天一閣的7130萬元(1億5686萬令吉),及來自百利宮的780萬元(1716萬令吉)額外租金收入)。

★投資收入:增79%,至1億4620萬元(3億2164萬令吉)(主要來自售出投資項目的淨利,及來自星和與第一通削減成本計劃的盈利)。 |

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 15-10-2007 12:14 PM

|

显示全部楼层

Singapore Press Holdings

BUY

Current Price: S$4.32

Target Price: S$5.00

FY07 Results

Singapore Press Holdings (SPH) reported its full year results. Net profit was up 18.1% to S$506.2m. However, after excluding exceptional gains of S$66.8m in FY06, net profits actually increased by 40%. Overall, results were in line with

expectations.

Maiden earnings contribution from Sky@eleven

SPH recognized approximately 11% of its profits for its property development project, the sky@eleven. SPH recognized S$71.3m in sales and S$94.8m in pre-tax profits for this project. Percentage of completion was higher than our expectations but profitability of the project was in-line with pre-tax margins at 67.1%.

Print revenue and property exceeded expectations; other segments in-line

• Print revenue in 4Q07 increased by 11.2% yoy to S$184.4m

• Print revenue for FY07 increased by 7.2% S$725.1m

• Rental income from the Paragon in 4Q07 increased by 8.9% to S$27.7m

• Rental income from the Paragon in FY07 increased by 7.9% to S$106.5m

Management attributed the stronger than expected growth in print revenue to higher yields in advertising due to an increase in the proportion of colour advertisements. Rental income at the Paragon also improved due mainly on the back of the strong property segment. Going forward, management has indicated that they do not have any plans to sell the Paragon. EBITDA margins excluding the Sky@eleven for FY07 was 41.6% as compared to 41.8% in FY06 as increases in staff costs were in line with SPH’s higher operating profits and newsprint costs remaining largely unchanged.

Final & Special Dividend

SPH has declared a final one-tier tax exempt dividend of 9 Scents and a special one-tier tax exempt dividend of 10 cents. This brings the total dividend paid out for the year to 26 Scents, slightly below our expected full year pay out of 27 cents.

Maintain BUY: Target Price raised to S$5.35

We have raised our valuation of SPH to S$5.35 based on our sum-of-the-parts valuation. Based on the current share price and our earnings forecasts, SPH should offer investors a dividend yield of 7.1%, 7.4% and 7.6% in FY08, FY09 and FY10 respectively. Maintain BUY |

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 15-10-2007 12:15 PM

|

显示全部楼层

Singapore Press Holdings

BUY: Price: $4.48 Target: $5.84

FY07 results

Analyst: CHAN Choon Jit

Sky@eleven Adds Impetus

Recurring earnings boosted by Sky@eleven development

SPH reported recurring earnings (profit before investment income and exceptional items) of $434.2m (+20.2%). The maiden profit of $47.8m from sale of the Sky@eleven condominium was included in the recurring earnings. Excluding the Sky@eleven contribution, recurring earnings would still have grown 7%. FY07 full-year DPS of $0.26 is slightly below our forecast of $0.265.

Healthy economy bolstered print ad revenue

Print advertisement revenue continued to grow strongly. Newspaper advertisement revenue, which formed the bulk (92.7%) of print advertisement revenue, increased 6.8% yoy. In the last two quarters, however, newspaper ad revenue grew by a much stronger 10.2% in Q307 and 10.7% in Q407.

Forecasting low double-digit growth in recurring earnings

For FY08-10, we expect growth of recurring earnings, boosted by profit recognition from Sky@eleven, to be in the low double-digits. A key downside risk would be a slowdown of the domestic economy, while stronger-than-expected advertising volume (arising from the Singapore leg of the F1 race and the integrated resorts) could provide upside surprises.

Sustaining margins and investing in new media

SPH has reiterated its commitment to managing costs to sustain the margins of the core newspaper business while investing in new media platforms to pursue growth. The group has benefited from soft newsprint prices in FY07 and expects newsprint prices to remain stable in the near term. It is also continuing to actively expand into social networking sites (launched Omy in Sep 07), its online classified site (ST701 expanded in Oct 07) and online search directories (joint venture with Fung Choi in Oct 07). We think such investments are definitely a step in the right direction but do not expect them to contribute significantly in the near term.

Dividend play at a steal

The FY07 dividend payout as a percentage of recurring earnings is about 96%, lower than the 103% figure for FY05 and the 106% figure for FY06. Nevertheless, we forecast DPS of $0.32 in FY08 and have raised our target price from $5.39 to $5.84 (implied FY08 dividend yield of 5.5%). |

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 2-1-2008 01:34 PM

|

显示全部楼层

1. Singapore Press Holdings – Company Update (Chan Choon Jit)

Previous Day Closing price: S$4.50

Recommendation: BUY (maintained)

Target price: S$5.84 (maintained)

♦ 1Q08 results to be announced on 14 January 08

The growth rate of print advertisement revenue is a key figure to watch for.

♦ Slowing GDP growth in 4Q07

This may have led the growth of print advertisement revenue to slow. We forecast 8% growth in FY08.

♦ Acquisition of luxury titles in North Asia

To immediately extend SPH’s reach in North Asia. Not expecting material impact on FY08 EPS.

♦ Attractive dividend play in 2008

Boosted by profit recognition of Sky@eleven, we forecast bumper dividend of 32cts, translating into a 7.1% yield for FY08. |

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 15-1-2008 11:04 AM

|

显示全部楼层

Singapore Press Holdings

BUY

Current Price: S$4.60

Target Price: S$5.60

(Previous: S$5.40)

1QFY08: Robust 10.2% advertising revenue growth

SPH reported a net profit of S$111.9m (+1%) for 1QFY08. Net profit was flat due to lower income from investments.

Of SPH’s 1Q08 pre-tax profit of S$135.4m (+0.2% yoy), the Newspaper &

Magazine and Property segments contributed S$107.0m (+13% yoy) and

S$25.2m (+92%) respectively. The Newspaper & magazine segment has

made a roaring comeback since 3QFY07. 1QFY08 registered a strong

newspaper advertising growth of 10.2%, contributed by 7.9% and 14.3%

growth in display and classified ads respectively. 2HFY07’s strong

advertising growth momentum was sustained into FY08.

The Property segment benefited from higher contribution from Paragon

Shopping Mall and a full-year impact of Sky@eleven in FY08. The former

contributed an increase in revenue of S$1.8m whereas the latter S$16.1m.

However, SPH’s group PBT was dragged down by lower investment income

of S$9.8m compared with S$29.7m previously. This was due to the fair

valuation of investments being affected by recent volatility in financial markets.

In addition, the previous year’s investment income was boosted by higher

dividend income from MobileOne Ltd and profit from a capital reduction

exercise by Starhub Ltd.

On the cost side, newsprint cost declined 3% to S$29.4m in 1QFY08

compared with S$30.3m a year ago. Average newsprint charge-out price

was US$587/tonne compared with US$602/tonne previously. However, staff

cost rose 15% to S$78.6m due to a higher variable bonus provision in line

with continued improved profitability of the newspaper business, increased

headcount and annual salary increment. Other operating expenses of

S$41.3m were up 13% with increased business activity and inclusion of costs for new subsidiaries.

We raise our print revenue growth assumptions from 5% p.a. for FY08, FY09 and FY10 to 8% for FY08 and 6% each for FY09 and FY10. However, we reduce our FY08 and FY09 net profit forecasts by 8% and 5% to S$513m and S$547m on lower investment income. Our FY10 forecast is relatively unchanged. Despite our reduced FY08 and FY09 earnings forecasts, we raise our target price from S$5.40 to S$5.60, premised on a revised SOP valuation of S$5.58/share, which factors in a higher valuation for SPH’s newspaper & Magazine business.

SPH is a good defensive stock in times of uncertainty. Its core fundamentals are now supported by a healthy AR growth, Paragon’s rising rentals on the back of rising rentals in prime shopping locations in Singapore, a full-year earnings contribution from Sky@eleven and a high annual net dividend yield of 6-7% p.a. Maintain BUY. |

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 15-1-2008 11:07 AM

|

显示全部楼层

Singapore Press Holdings: Dividend play in volatile markets

Flatter than anticipated. SPH reported its 1Q08 results yesterday with topline rising 8.2% YoY to S$261.3m and net profit inched ahead 1.1% YoY to S$111.9m. Lower than expected lumpy recognition from the Sky@Eleven project caused SPH to miss our net profit forecasts by about 14%. Investment income was also affected by volatility in the financial markets and one-off items and thus came in 66.9% YoY lower at S$9.8m.

Stretching on Singapore's economy. SPH continues to stretch its growth on the back of Singapore's economy. Its core business of newspapers and magazines grew 8.2% YoY, closely mimicking Singapore's 2007 GDP growth of 7.5%. The Singapore government forecasts the economy to grow at 4.5-6.5% for 2008 and we expect this moderate expansion to support SPH's core business as Singapore's dominant newspaper provider.

Flexibility that costs. In the rapidly evolving digital age, the need to remain nimble and relevant towards its readers has been highlighted as one of SPH's priorities. However, retaining good talent and developing new businesses to go beyond print in Singapore has resulted in staff costs rising 14.7% YoY to S$78.6m due to better compensation and a 5.8% YoY increase in headcount to 3,771 staff.

Pylons of support. Paragon will also be going through a makeover with two new floors for medical suites/offices along with increased commercial NLA by 11,600 sqft. This renovation will cost S$82m and is expected to be completed by end 2008. Paragon continues to attract top luxury brands and we expect rentals to remain buoyant to support SPH's revenue.

Safe haven in volatile markets. Although we have mitigated our expectations on investment returns as guided by SPH, we are encouraged that SPH's core business continues to match the Singapore economy's growth pace and are mindful that bottomline will be supported by recognition from its Sky@Eleven project. Assuming a similar payout ratio as previous years, we estimate that the stock's dividend yield could be 5.7% in FY08, making SPH an attractive defensive play for a shaky market. We revise our fair value to S$5.14 (prev: S$4.87) using SOTP valuation. Upgrade to BUY.

|

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 19-3-2008 01:50 PM

|

显示全部楼层

Singapore Press Holdings

BUY

Current Price: S$4.51

Target Price: S$5.60

2QFY08’s advertising revenue growth could surprise on the upside SPH will be releasing its 2QFY08 (Dec 07-Feb 08) results on 14 April. Advertising revenue growth could surprise on the upside. Our page-counts of the Straits Times are indicating an advertising growth of 5.2% yoy in 2QFY08, advertising revenue growth. Including the impact of an advertising rate increase of about 2% effective from Jan 08, advertising revenue growth could come in higher. Display ad rates for The Straits Times have been raised by 7.5%, while The Sunday Times has seen a 3-4% increase for notices and classifieds. Separately, ACNielsen data is indicating SPH’s advertising revenue growth at a whopping 13.8% yoy for Dec 07 and Jan 08 combined, This strong growth could be due to a seasonally impact of early advertising by advertisers as 2008’s lunar new year was in early February compared with a mid-Feb lunar new year in 2007.

Historically, both our page-counts and ACNielsen data were good in guiding advertising revenue trends, but were not necessarily accurate in guiding the absolute growth figures. Nevertheless, SPH’s 1QFY08 advertising revenue growth of 10.2% yoy was higher than both our estimate of a 5.7% yoy growth (based on our page-counts) and ACNielsen’s estimate of 7.7% yoy growth.

We look forward to a decent advertising revenue growth to be reported by SPH for 2QFY08. In our earnings forecasts, we are assuming a print revenue growth of 8% for FY08 and 6% each for FY09 and FY10.

The size of investment income remains a potential negative in 2QFY08 results as Singapore stock-market has been in a sharp correction since October last year. Investment income in 1QFY08 was below expectation. We view this a short-term negative.

SPH has outperformed the market since 4Q07 with a positive absolute return (including dividends). In the current sharp market correction, SPH is standing tall while most stocks have fallen off the cliff. SPH’s core fundamentals are now supported by a healthy AR growth, Paragon’s rising rentals on the back of rising rentals in prime shopping locations in Singapore, a full-year earnings contribution from Sky@eleven in FY08 and a high annual net dividend yield of 6-7% p.a. Maintain BUY. |

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 8-4-2008 11:21 AM

|

显示全部楼层

Singapore Press Holdings (SPH), through SPH Interactive International Pte Ltd (SPH II), has forged a joint venture (JV) with Star Publications (Malaysia) to provide digital media services in Malaysia. The JV is called 701Panduan Sdn Bhd. In Malay, panduan

means to provide direction or guidance, which is what 701Panduan aims to do by helping consumers find what they need on new media platforms. The authorised and paid-up capital of 701Panduan is RM60 million (S$26 million), with SPH II and Star Publications each holding 50%. The deal was signed yesterday at the headquarters of Star Publications in Kuala Lumpur, Malaysia. Star Publications publishes The Star, Malaysia's most widely read English daily. (BT)

|

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 22-4-2008 05:51 PM

|

显示全部楼层

Singapore Press Holdings (S$4.43) - 2QFY08 results - Still going strong

In line. 2QFY08 earnings of S$99.6m (-6.2% yoy) were led by strong advertising revenues (+11.4% yoy) and a S$17m earnings contribution from sky@eleven. The strong core performance was partially eclipsed by weaker-than-expected investment income (-48% qoq) due to weaker financial markets. 1HFY08 earnings have now met 40% of our full-year forecast and consensus (SPH’s second half is typically stronger). An interim dividend of 8.0 Scts/share (+1.0 Sct yoy) was announced.

Robust 18.9% yoy revenue growth. 2QFY08 core revenue (excluding sky@eleven’s S$24.2m contribution) grew 9.3% yoy, driven by strong advertising revenue (+11.4% yoy). This marked the fourth consecutive quarter of double-digit adex growth as SPH rode the tailwinds of a strong domestic economy. Property rental revenue grew 10% yoy as Paragon enjoyed rental reversions. Circulation revenue was flat (-1.1% yoy).

2QFY08 EBITDA margin expanded to 44.1% (+350bp yoy), benefiting from operating leverage at core operations and contributions from the higher-margin sky@eleven project. Robust topline growth helped SPH stay ahead of staff costs which rose 9.7% yoy on headcount increases and salary increments. SPH also benefited from weaker newsprint costs (US$575/tonne, -5% yoy) during the quarter.

No signs of weakness yet. The impact of slowing global growth has yet to bite into adex demand. SPH continues to benefit from a tight labour market, as can be seen in its strong classifieds performance (+15% yoy). We believe Singapore’s economy remains wellsupported by an immigration boom, the rollout of two integrated resorts and Singapore’s rise as a key global destination for business and leisure travellers.

Reducing earnings estimate. Our FY08 earnings estimate has been trimmed by 5.5% to account for lower investment returns amid weakness in the financial markets and an intentional shift towards a more conservative portfolio.

Maintain Outperform and sum-of-the-parts target price of S$5.20. In view of heightened market risk aversion, we continue to expect SPH to outperform the index on reliable earnings from its print-media monopoly, revenue recognition of sky@eleven,

exposure to Singapore’s adex growth and a solid CY08 dividend yield of over 7%. |

|

|

|

|

|

|

|

|

|

|

|

发表于 12-8-2008 11:52 AM

|

显示全部楼层

发表于 12-8-2008 11:52 AM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 28-9-2008 01:32 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 5-9-2009 11:03 PM

|

显示全部楼层

没有SPH的消息了吗?和我平岁的你....好想买你来收.. |

|

|

|

|

|

|

|

|

|

|

|

发表于 10-7-2012 08:42 PM

|

显示全部楼层

本帖最后由 icy97 于 10-7-2012 08:55 PM 编辑

最近这个股突然上到4块。。。

可是却没有看到任何dividend的消息哦。。

因为根据以往,都是有dividend之前 才会上升的很快。。。

不过到现在 还突不破这个4块钱的点。。。

上次年中的时候 也是到4块 就往回跌了。。

不过有看到报道说 有一个合股开发的SPH magazines即将上市。。。

不知道是不是这个的缘故。。。毕竟SPH是大股东。。。 |

|

|

|

|

|

|

|

|

|

|

|

发表于 14-7-2012 10:33 AM

|

显示全部楼层

发表于 14-7-2012 10:33 AM

|

显示全部楼层

报业控股第三季 经常性盈利增2.2%

http://www.zaobao.com/cs/cs120714_006_1.shtml

(2012-07-14)

报业控股执行总裁陈庆鏻表示,平面广告收入的起伏,将会继续和新加坡的经济表现同步。集团也将在力求核心报章业务表现可持续的同时,继续积极争取增长的机会。

房地产业务的强劲表现,带动了新加坡报业控股(SPH)的经常性盈利(recurring earnings),第三个财政季度经常性盈利比去年同期增加2.2%至1亿1264万元。营运收入增加0.9%至3亿3184万元。

报业控股昨天公布,2012财年第三季的税后净利为9978万元,比上财年第三季下跌13.1%。这主要是因为投资收入受到金融市场波动影响,这个财政季度的投资收入下降了59.9%至950万元。

核心的报章与期刊业务在这段期间的收入微跌0.6%,至2亿6140万元;平面广告收入稍微下跌0.4%至2亿零180万元;发行收入则下滑3.6%至5180万元。

第三季的每股盈利为6分,截至5月底的每股净资产值是1.33元。

报业控股是在昨天股市闭市后,发布了截至今年5月底的第三季业绩。

房地产业务方面,租金收入增加12.8%至4870万元。金文泰广场(Clementi Mall)的租金收入增加了58.6%至950万元,这是因为去年第三季时该商场尚未全面运作。来自百利宫(Paragon)的租金收入,也随着租金上调增加了5.3%。

集团其他业务的营业收入下滑4.1%至2180万元,主要是因为展览业务收入下降所导致。

在成本方面,由于印刷量减少了,让新闻纸成本减少了5.1%。另一方面,员工成本则增加6.8%,主要是因为工资增加、为员工的可变动花红拨出较高的准备金以及收购ACP Magazine带来的员工人数增加所导致。

其他营业开支因为派发成本和促销活动等商业活动涉及的开支,增加了7.0%。

在截至5月31日的前九个月内,集团的经常性盈利为3亿2390万元,比去年多了6.1%。营运收入增加2.9%而总营运开销上升1.6%。

九个月投资收入下跌63.8%,而归属股东净利比去年同期则少了1110万元或3.8%,报2亿8140万元。

对于2012财年的展望,董事会表示,排除无法预见的因素,预计本财年的业绩将会是令人满意的。

报业控股执行总裁陈庆鏻说:“平面广告收入的起伏,将会继续和新加坡的经济表现同步。集团将在力求核心报章业务表现可持续的同时,继续积极争取增长的机会。”

他也表示,由于目前金融市场动荡,集团选择了一个比较保守的投资组合的资产分配,因此回报率也预计将与这个较低的风险状况相称。

报业控股昨天闭市上涨3分或0.75%,收报4.02元。 |

|

|

|

|

|

|

|

|

|

|

|

发表于 23-8-2012 11:13 AM

|

显示全部楼层

报业控股盛港西项目 命名为"利达广场"

http://www.zaobao.com.sg/cs/cs120823_014.shtml

(2012-08-23)

新加坡报业控股(SPH)与联合工程(United Engineers)合资在盛港西发展的商场,正式命名为“利达广场”(The Seletar Mall)。

合资双方是在2012年1月中标到建屋发展局售卖的盛港西商业地段,该99年地契地段位于盛港西道和芬维尔路交界处。

报业控股和联合工程分别持有利达广场70%和30%股权。利达广场预期将在2014年底落成。

|

|

|

|

|

|

|

|

|

|

|

|

发表于 12-10-2012 11:39 PM

|

显示全部楼层

SPH posts 5.9% lower full-year net of $365.5m

http://www.theedgesingapore.com/the-daily-edge/business/40539-sph-posts-6-lower-full-year-net-of-366m.html

Fri, 12 Oct 18:56

Singapore Press Holdings reported a net profit of $365.5 million for the year ended Aug 31, 5.9% lower compared to the previous year.

Group recurring earnings were $410.2 million for the year, or 0.3% higher as growth in the property and exhibitions businesses offset the lower profits from the newspaper and magazine segment.

Group operating revenue of $1.27 billion was 1.8% higher compared to the previous year. Revenue for the group's newspaper and magazine business was $1 billion. |

|

|

|

|

|

|

|

|

|

|

|

发表于 13-10-2012 01:12 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 15-10-2012 02:01 PM

|

显示全部楼层

Singapore Press Holdings yield still attractive-brokers

http://www.theedgesingapore.com/the-daily-edge/business/40550-singapore-press-holdings-yield-still-attractive-brokers.html

Mon, 15 Oct 12:28

Singapore Press Holdings still offers an attractive yield even after the media and property firm reported

a 5.9% fall in 2012 net profit mainly due to lower investment income, brokers said.

SPH shares were up 0.5% at S$4.09 on Monday. The stock has risen nearly 11% so far this year versus the 15% gain in the broader Straits Times Index.

SPH posted net profit of S$365.5 million ($299.3 million) for its financial year ended August, down 5.9% from a year earlier. The company announced full-year dividend of 24 Singapore cents, representing a yield of nearly 6%.

Maybank Kim Eng said the yield spread between SPH and 10-year government bond is now 443 basis points (bps), above the historical average of 350 bps.

The broker expects SPH to declare a dividend of 25 cents for 2013 fiscal year, implying yield of 6.2% which it said is still very attractive. Maybank raised its target price to $4.50 from $4.43 and kept its ‘buy’ rating.

CIMB Research, which has an ‘outperform’ rating and $4.39 target price, said SPH’s property business remains the star performer and could help drive dividend payout in 2013. Both Paragon and Clementi malls had rental increases this year, CIMB noted.

OCBC Investment Research said falling margins highlighted the increasing uncertainties for SPH’s core print business, but SPH’s dividend yield is likely to limit the share price downside. OCBC has a ‘hold’ call and $4.05 target price.

PH's dividend yield remains attractive: Maybank-KimEng

http://www.theedgesingapore.com/the-daily-edge/business/40545-sphs-dividend-yield-remains-attractive-maybank-kimeng.html

Mon, 15 Oct 10:16

Singapore Press Holdings’ FY12 results were broadly in line with expectations, Maybank-Kim Eng says, noting revenue rose 1.8% on year to $1.27 billion on a strong property segment performance, while core earnings rose 0.3% on year.

It notes FY12 core print advertisement revenue dropped 1% on year on weak economic conditions; the house expects a FY13 ad revenue bottom. The property segment will drive growth ahead, with FY12 rental income +12.8% on year at $191.4 million on higher rentals at Paragon and the Clementi Mall’s full operation, it says; “as Clementi Mall has not achieved its maximum rental rate and demand in Orchard Road remains robust, we believe there is still upside from property rental income for FY13.”

It notes the operating-profit margin was a healthy 32% as costs were well-managed; Maybank-KE is confident a 30% margin is sustainable. While FY12’s $0.24/share dividend was flat on year, it expects FY13’s dividend at $0.25/share, implying a “still attractive” 6.2% yield, offering the stock downside protection; “more upside can be expected if a spin-off of Paragon and Clementi eventuates.” It raises its target to $4.50 from $4.43, keeping a Buy call. The stock is up 0.3% at $4.08.

UOB-KayHian downgrades SPH to Hold, trims target

http://www.theedgesingapore.com/the-daily-edge/business/40575-uob-kayhian-downgrades-sph-to-hold-trims-target.html

Mon, 15 Oct 15:15

UOB KayHian downgrades Singapore Press Holdings to Hold from Buy after the company reported newspaper advertising revenue contracted 5.7% on-year in 4Q12, compared with 3Q12’s 1.3% on-year contraction.

“Traditionally, SPH’s share price has a close relationship with its newspaper AR growth. We see weak AR growth capping share price performance, but this is compensated by an attractive dividend yield of 5.4% (for FY13-15). In today’s global anaemic growth and low interest-rate environment, yield stocks still find favour among investors.”

It cuts its target to $4.30 from $4.50 after revising its sum-of-the-parts valuation; it lowers its FY13-14 earnings forecasts by 8%-10% on lower projected revenue and higher depreciation. The house tips a $3.80 entry price. The stock is up 1% at $4.11.

Citi downgrades SPH to 'sell' from 'buy'

http://www.theedgesingapore.com/the-daily-edge/business/40592-citi-downgrades-sph-to-sell-from-buy-.html

Tue, 16 Oct 12:06

Citigroup downgraded print and property company Singapore Press Holdings to ‘sell’ from ‘buy’ and cut its target price to $3.80 from $4.15 on weaker-than-expected quarterly earnings and slower growth prospects for the next year.

Shares of SPH were down 0.5% at $4.09, but have risen 10.8% since the start of the year, compared to the Straits Times Index's 15.4% gain.

SPH posted net profit of $365.5 million for its financial year ended August, down 5.9% from a year earlier.

Citi said SPH's fourth-quarter net profit of $84 million was weaker than expectations, due to poor print ad sales, falling circulation demand and rising cost pressures.

Citi cut its 2013-2014 earnings estimates for SPH by 8-11%, reflecting the company's challenges to grow its core media business in Singapore as classified and circulation segments continue to decline.

“We think demand for print ads is unlikely to pick up strongly amid moderate growth expectations in 2013 and a lackluster structural outlook for circulation,” said Citi in a report. 本帖最后由 icy97 于 16-10-2012 01:08 PM 编辑

|

|

|

|

|

|

|

|

|

|

| |

本周最热论坛帖子 本周最热论坛帖子

|

2894

2894  99

99