|

|

楼主 |

发表于 17-6-2008 07:16 PM

|

显示全部楼层

献给对行为金融学有兴趣的朋友~

http://www.geocities.com/francorbusetti/behavioural.htm

| A quick and easy introduction | Daniel Kahneman,

Mark Riepe | An excellent and succinct introduction to the topic from one of its leading exponents. The examples are both fun and instructive in establishing just how flawed your investment thinking may be and the paper offers some pragmatic recommendations to market practitioners on how to deal with these traits in oneself and one's clients. | | | | | | Behavioural finance

and the sources of alpha | Russell Fuller | Behavioral finance is a new field in economics that has recently become a subject of significant interest to investors. This article provides a general discussion of behavioral finance and presents some insights from this field that apply to the problems plan sponsors face when evaluating and selecting active equity managers. | | | | | | Why women are better traders than men... | Brad Barber,

Terrance Odean | Theoretical models predict that overconfident investors trade excessively. We test this prediction by partitioning investors on gender. Psychological research demonstrates that, in areas such as finance, men are more overconfident than women. Thus, theory predicts that men will trade more excessively than women. Using account data for over 35,000 households from a large discount brokerage, we analyse the common stock investments of men and women from February 1991 through January 1997. We document that men trade 45 percent more than women. Trading reduces men’s net returns by 2.65 percentage points a year as opposed to 1.72 percentage points for women. | | | | | | Are strategists reliable contrary indicators? | Kenneth Fisher,

Meir Statman | Investors are not all alike and neither is their sentiment. The sentiment of Wall Street strategists is unrelated to the sentiment of individual investors or that of newsletter writers although the sentiment of the last two groups is closely related. Sentiment can be useful for tactical asset allocation. There is a negative relationship between the sentiment of each of the three groups and future stock returns and that relationship is statistically significant for Wall Street strategists and individual investors. | | | | | | Behavioural portfolio construction | Hersh Shefrin,

Meir Statman | We develop a positive behavioral portfolio theory and explore its implications for portfolio construction and security design. Portfolios within the behavioral framework resemble layered pyramids. Layers are associated with distinct goals and covariances between layers are overlooked. We explore a simple two-layer portfolio. The downside protection layer is designed to prevent financial disaster. The upside potential layer is designed for a shot at becoming rich. Behavioral portfolio theory has predictions that are distinct from those of mean-variance portfolio theory. In particular, behavioral portfolio theory is consistent with the reluctance to have short and margined positions, an inverse relation between the bond/stock ratio and portfolio riskiness, the existence of the home bias, the use of labels such as “growth” and “income,” the preference for securities with floors on returns, and the purchase of lottery tickets. | | | | | | The frailties of forecasting | Kenneth Fisher,

Meir Statman | Tactical asset allocation practitioners emphasise quantitative tools, while traditional market timing practitioners emphasise qualitative ones. Each forecasting method is subject to biases and each calls for remedies.This paper discusses five cognitive biases that underlie the illusion of validity: overconfidence, confirmation, representativeness, anchoring and hindsight. In this short, very readable document the authors use forecasts based on p/e ratios and dividend yields to illustrate these biases and offer remedies. | | | | | | Learning to let go | Terrance Odean | This paper examines the so-called disposition effect, the tendency of investors to hold losing investments too long and sell winning investments too soon. They may (rationally or irrationally) believe that their current losers will in future outperform their current winners. Unfortunately, the winning investments that they choose to sell continue in subsequent months to outperform the losers they keep. This results in poor returns, particularly in taxable situations. The paper does not, however, suggest methods of counteracting this aberrant behaviour. Clearly, rigorous internal investment processes, which include profit-taking and loss-taking rules, are required. | | | | | | Why so many earnings surprises? | David Dreman | This paper presents typical analyst forecast errors by industry and shows that these errors are large and related to behavioural tendencies towards extrapolation from the past, being misled by expert opinion and consensus as well as peer and institutional pressures. He examines the different types of earnings surprises, their impact, size and frequency and finds that there is post-surprise reversion towards the mean. Analysts and fund managers typically display the behavioural phenomenon of unjustified confidence. When this is betrayed by a surprise the result is overreaction, which results in the long-term success of contrarian strategies. | | | | | | Can investors profit from the prophets? | Brad Barber,

Reuven Lehavy,

Maureen McNichols,

Brett Trueman | In this paper we document that stocks highly recommended by analysts outperform the market, while those that are unfavourably recommended underperform. Our findings are based on an extensive analysis of over 360,000 analyst recommendations from 269 brokerage houses over the period 1986-1996. We show that strategies of purchasing the stocks with the most favourable consensus (average) recommendations or selling short those with the least favourable recommendations, in conjunction with daily portfolio rebalancing and a quick investor response to changes in consensus recommendations, yielded an annual abnormal gross return of more than 4 percent. Less frequent portfolio rebalancing or a delay in reacting to consensus recommendation changes diminished the abnormal returns; however, they did remain significant for the least favourably rated stocks. We also show that quite high trading levels are required to capture the excess returns generated by the strategies we analyse, entailing substantial transactions costs and leading to abnormal net returns that were not reliably greater than zero. |

[ 本帖最后由 蚂蚁小弟 于 17-6-2008 07:26 PM 编辑 ] |

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 17-6-2008 07:24 PM

|

显示全部楼层

| The need for behavioural finance | Werner De Bondt | The paper outlines how behavioural finance is needed to address the problem of Keynes' "animal spirits" (i.e. sentiment), which distorts modern finance theory as a result of aberrations such as "bounded rationality" (i.e. people are silly sometimes), the fact that mistakes are repeated (by many people at the same time or the same people at different times), that false beliefs do matter and that information is not always asymmetrical (i.e. silly people may not be aware that they are being silly). It discusses the concepts of framing, heuristics and the dynamics of security prices, including analyst forecasts, the winner/loser effect and evidence of market underreaction. | | | | | | All the phenomena of behavioural finance | Robert Shiller | Recent literature in empirical finance is surveyed in its relation to underlying behavioral principles, principles which come primarily from psychology, sociology and anthropology. The behavioral principles discussed are: prospect theory, regret and cognitive dissonance, anchoring, mental compartments, overconfidence, over- and underreaction, representativeness heuristic, the disjunction effect, gambling behavior and speculation, perceived irrelevance of history, magical thinking, quasi-magical thinking, attention anomalies, the availability heuristic, culture and social contagion, and global culture. | | | | | | People are normal, not rational! | Meir Statman | the attached article compares behavioural finance with standard finance. Standard finance is a poor descriptive theory of finance. Investors regularly overlook the arbitrage principles of Miller and Modigliani, fail to use Markowitz in constructing their portfolios and don't drive stock returns to levels predicted by Sharpe’s CAPM. People in standard finance are rational whereas people in behavioural finance are not always rational, but are always normal. Normal people are often confused by frames, are affected by cognitive errors, know the pain of regret and the struggle with self-control. Statman discusses the puzzles of investor's preference for cash dividends, the phenomena of selling winners too early and riding losers too long, the pursuit of "popular" stocks, the role of marketing financial products and the behavioural forces that shape financial regulations. | | | | | | Homo Economicus flawed | Sendhil Mullainathan,

Richard Thaler | Some of the interesting anomalies discussed include: There are important limits to arbitrage - it may often pay “smart money” to follow “dumb money” rather than to lean against it. There are limits to learning – the opportunity costs of learning or experimenting can result in us becoming stuck in nonoptimal equilibrium, simply because the cost of trying something else is too high. A rapidly-changing environment exacerbates this, and learning opportunities can be limited to start with - for example, the number of times we get to learn from our retirement decisions is low, and possibly zero. The three tenets of the so-called “standard economic model” of human behaviour: unbounded rationality, unbounded willpower and unbounded selfishness are all called into question, as are core economic principles such as the law of one price. The article illustrates some of these aspects in a field we have not touched on before: savings. For example, the life cycle model of savings and consumption is patently untrue, as illustrated by the frightening fact that most people cannot afford to retire. | | | | | | The best value strategies | Lakonishok,

Schleifer, Vishny | The paper shows that a wide range of value strategies do indeed produce higher returns, and then tackles the two potential explanations. It shows that the pattern of returns and the structure of past, expected and actual growth rates is consistent with the contrarian model, and that there is little, if any, support for the view that value strategies are fundamentally riskier. The resulting implication is that the market has a predilection for naive growth strategies. Reasons for this could be the placing of excessive weight on recent history, "glamour" factors, the overestimation of good but expensive companies and the very pertinent fact that most investors have shorter time horizons than are required for value strategies to pay off consistently. | | | | | | Why do we do it? | Richard Thaler | The article examines the reasons that lead to the rise of behavioural finance. These were generally anomalies inexplicable by conventional financial economics theory, such as excessive trading, excessive volatility, the dividend puzzle, the equity premium puzzle and the predictability of returns. He then summarises the progress and discoveries made by the behavioural approach and suggests further areas of investigation. These include large-cap stocks, corporate finance and the behaviour of individual investors. | | | | | | The unbearable asymmetry of newsflow | Jennifer Conrad,

Bradford Cornell,

Wayne R. Landsman | We examine whether the asymmetrical price response to bad and good earnings shocks changes as the relative level of the market changes. The study is based on a sample of 24,108 announcements of firms’ annual earnings during the period 1988 to 1998. The level of the market is a relative measure based on the difference between the market P/E at the end of the announcement month and the average market P/E over the prior 12 months. Predictions based on behavioral finance models and extended regime-shifting models suggest that stock prices should respond more strongly to negative news as the relative market level rises. Similarly, prices should respond more strongly to good news in bad times, although the effect should be somewhat attenuated if the regime-shifting models are descriptively valid. The findings generally support these predictions. |

|

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 17-6-2008 07:25 PM

|

显示全部楼层

| The assimilation of behavioural finance | George Frankfurter,

Elton McGoun | In this paper we compare and contrast modern finance (the de facto ruling paradigm of financial economics) with what is being called (most of the time) behavioral finance, and some time “the anomalies literature.” The faithful of the ruling paradigm have marginalised behavioral finance by making it the “anomalies literature.” But even the supposed proponents of behavioral finance are marginalising themselves by clinging to the underlying tenets, forms, and methods of what is now called modern finance. They have allowed it to set the terms of the debate and made it the benchmark against all finance is not only judged, but also labelled “finance.” But finance research is subject to the same “mistakes” that behavioral finance attributes to practitioners, and it is these same “mistakes,” perhaps more than the fierce attacks of the supporters of the ruling doctrine that are preventing behavioral finance from emerging as a new paradigm. In effect, the mere failure of behavioral finance is proof of its veracity and legitimacy. | | | | | | Investor Psychology in Capital Markets | Kent Daniel,

David Hirshleifer,

Siew Hong Teoh | We review evidence about how psychological biases affect investor behavior and prices. Systematic mispricing probably causes substantial resource misallocation. We argue that limited attention and overconfidence cause investor credulity about the strategic incentives of informed market participants. However, individuals as political participants remain subject to the biases and self-interest they exhibit in private settings. Indeed, correcting contemporaneous market pricing errors is probably not government’s relative advantage. Government and private planners should establish rules and procedures ex ante to improve choices and efficiency, including disclosure, reporting, advertising, and default-option-setting regulations. Especially, government should avoid actions that exacerbate investor biases. | | | | | | Trading Places | Lawrence Harris | The paper introduces the topic by stating that on any given transaction, the chances of winning or losing may be near even. However, in the long term winners profit from trading because they have some persistent advantage which allows them to win slightly more often, or slightly bigger, than the losers. Winners choose better portfolios than losers, they time their trades better than they negotiate their trades better. The paper examines the economics that determine the winners and losers in trading, the types of traders and how their trading styles lead to profits or losses as well as how access to information of various types creates trading advantages and why many losing traders continue to trade. | | | | | | An Unflattering Portrait | Werner De Bondt | The article offers a brief survey of prior research and produces new survey evidence of actual investor behaviour, offering a list of widely-acknowledged anomalies in behaviour as well as some interpretations. Four classes of anomalies are discussed: Investors' perceptions of the stochastic process of asset prices, investors' perceptions of value, the management of risk and return and trading practices. The portrait of investors which develops is unflattering. | | | | | | Contrarian and Momentum Strategies | Dirk Schiereck,

Werner de Bondt,

Martin Weber | The research analysed the profitability of these two strategies on the Frankfurt Stock Exchange over 31 years. It found that both strategies were profitable and examined some possible reasons, including the size effect and various risk measures, including the macroeconomic environment. Interestingly, the momentum strategies performed well irrespective of the state of the economy, while the contrarian strategies performed poorly when the discount rate was low and when long-term interest rates greatly exceeded short-term rates. | | | | | | Investor Sentiment and

Asset Valuation | Gregory W Brown,

Michael T Cliff | The attached paper tests two main hypotheses. The first is that excessive optimism leads to periods of market overvaluation. This would then lead to the second hypothesis, that high current sentiment is followed by low cumulative long-run returns as the market price reverts to its intrinsic value. If the price correction were quick and predictable, there would be a potentially profitable trading strategy. It is found that after a bullish shock to sentiment there is an economically significant positive effect on prices in the first few months, which is then nearly completely reversed over the next three years. This effect is concentrated in the large-cap growth stocks. | | | | | | Herd Behaviour and

Cascading in Capital Markets | David Hirshleifer,

Siew Hong Teoh | The attached paper reviews both fully rational and imperfectly rational theories of behavioural convergence; their implications for investor trading, managerial investment and financing choices, analyst following and forecasts, market prices, market regulation and welfare; and associated empirical evidence. Some of the more interesting sections deal with herd behaviour in research and trading, herding by stock analysts and other forecasters and cascading effects in securities trading, creditor runs, bank runs, financial contagion and crashes. | | | | | | Brain Hemispheric Consensus | Michael Boyd | Are you primarily left-brained or right-brained? And will this have any effect on your investment performance? In this rather fun paper Michael Boyd reports on the result of an experiment he carried out on his MBA students. The experiment seemed to support the view that hemispheric consensus may lead to better stock selection, but not necessarily to the extent of outperforming an unmanaged index. Moreover, it appears likely that the technique’s benefits quickly dissipate with the passage of time. It may therefore follow that hemispheric consensus building is better applied to active portfolio management or even short-term trading than to buy-and-hold strategies. |

|

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 17-6-2008 07:29 PM

|

显示全部楼层

原文+链接转帖希望版主通融

方便小弟和其他人日后慢慢下载来刨 |

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 17-6-2008 07:39 PM

|

显示全部楼层

贴现现金流量法

贴现现金流量法出自MBA智库百科(http://wiki.mbalib.com/)(重定向自现金流贴现模型)

贴现现金流量法(拉巴波特模型,Rappaport Model,DCF法)

[编辑]

什么是贴现现金流量法 贴现现金流量法是由美国西北大学阿尔弗雷德·拉巴波特于1986年提出,也被称作拉巴波特模型(Rappaport Model),是用贴现现金流量方法确定最高可接受的并购价值的方法,,这就需要估计由并购引起的期望的增量现金流量和贴现率(或资本成本),即企业进行新投资,市场所要求的最低的可接受的报酬率。

该模型所用的现金流量是指自由现金流量(Free Cash Flow,简写FCF)即扣除税收、必要的资本性支出和营运资本增加后,能够支付给所有的清偿者的现金流量。

用贴现现金流量法评估目标企业价值的总体思路是:估计兼并后增加的现金流量和用于计算这些现金流量现值的折现率,然后计算出这些增加的现金流量的现值,这就是兼并方所愿意支付的最高价格。如果实际成交价格高于这个价格,则不但不会给兼并企业带来好处,反而会引起亏损。

[编辑]

运用贴现现金流量法的步骤 运用贴现现金流量法需经过三个步骤:

第一步,建立自由现金流量预测模型。

拉巴波特认为有五种价值动因影响目标企业的价值,即销售增长率、经济利润边际、新增固定资产投资、新增营运资本、边际税率等。他把这五种因素运用在自由现金流量模型中,公式表述为:FCF=S[,t-1](1+g[,t])·P[,t](1-T)-(S[,t]-S[,t -1])·(F[,t]+W[,t])。

其中:FCF——自由现金流量;S[,t]——年销售额;g[,t]——销售额年增长率;P [,t]——销售利润率;T——所得税率;F[,t]——销售额每增加1元所需追加的固定资本投资;W[,t]——销售每增加1元所需追加的营运资本投资;t——预测期内某一年度。

第二步,估计折现率或加权平均资本成本。

折现率是考虑了投资风险后,兼并方要求的最低收益率,也就是该项投资的资本成本。这里所指的资本成本不是并购方企业自身的加权资本成本,而是并购方投资于目标企业的资本的边际成本。由于并购方用于并购的资金来源是复杂的,可能来自留存收益、增发新股,也可能是举债融资,这就需要对各种各样的长期资本成本要素进行估计,并计算加权平均资本成本。其中,自有资金的成本可用资本资产定价模式求得,而债务成本则可用债务利息经税务调整后的有效资本成本得到。最后,该项投资的资本成本就是这二者的加权平均,也就是平均资本成本(K),即:K=Ks(S/V)+Kb(1-T)(B/V)。其中:Ks——股东对此次投资要求的收益率;Kb——利率;S——自有资金数量;B——对外举债;V——市场总价值;T——企业的边际税率。

第三步,利用贴现现金流量模型,计算现金流量的现值。

V=∑(FCF/(1+K)[t])+(F/(1+K)[t])

其中,FCF——自由现金流量;K——折现率或加权平均资本成本;F——预期转让价格;V——企业价值。

[编辑]

贴现现金流量法的作用与局限性 贴现现金流量法以现金流量预测为基础,充分考虑了目标公司未来创造现金流量能力对其价值的影响,在日益崇尚"现金至尊"的现代理财环境中,对企业并购决策具有现实的指导意义。但是,这一方法的运用对决策条件与能力的要求较高,且易受预测人员主观意识(乐观或悲观)的影响。所以,合理预测未来现金流量以及选择贴现率(加权平均资本成本)的困难与不确定性可能影响贴现现金流量法的准确性。

来自"http://wiki.mbalib.com/wiki/%E8%B4%B4%E7%8E%B0%E7%8E%B0%E9%87%91%E6%B5%81%E9%87%8F%E6%B3%95" |

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 17-6-2008 07:39 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 17-6-2008 07:40 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 17-6-2008 07:43 PM

|

显示全部楼层

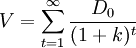

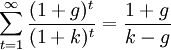

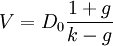

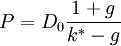

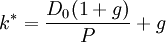

股票内在价值的计算方法

为简便起见,在不会影响到计算结果的理论含义的前提下,人们通常把上述各种收益简而归之为股利。下面就是股票内在价值的普通计算模型:

计算公式:V=∑dt/(1+k)t

其中, V ……内在价值

dt……第t年现金流入

k ……贴现率,则(1+k)t为第t年贴现率

“宁肯要模糊的正确,也不要精确的错误”,先引用一下巴菲特的名言,体现在公式里面就是两个因子的不确定性,对于dt和k的选取,如何做到模糊的正确,是问题的核心所在。

关于dt:

- 对于t<0的情况,反映的是历史的现金流入情况,如果财务没有作假的话,那么可以很容易从公司历年年报中获得

- 对于t=0的情况,有大量的行业分析报告和公司分析报告,d0相对来说可以比较准确

- 对于t>0的情况,t取值越大,意味着预测年度距离当前越远,而影响公司现金流入的因素颇为复杂,那么精确预测尤为困难。

关于贴现率k:

- 贴现率就是用于特定工程资本的机会成本,即具有相似风险的投资的预期回报率

- 按照贴现率的定义,选取社会平均资本回报率作为贴现率是恰当的

- 1992年~2003年的社会资本平均回报率在9~10%间波动(参考《中国统计年鉴》(1987-2003))

- k值对内在价值的影响很大,个人认为采用10%作为k值引入计算是合理的

- 关于k的取值,有人采用的是5年期债券收益率加上一个安全率,个人认为不太妥当,首先,安全率是一个很模糊的取值,而没有参考依据,如果太高会导致与优秀的公司擦肩而过,如果太低,则很可能会对内在价值严重高估。那么据此投资的结果将是灾难性的。

这是计算股票内在价值的最基本公式,但要注意,这也是唯一的真实公式,在计算各种简化模型的时候都是建立在各种特定假设的基础之上。在现实分析中运用简化模型的时候,应该时刻不要忘记这个真实的公式。

来自"http://wiki.mbalib.com/wiki/%E8%82%A1%E7%A5%A8%E5%86%85%E5%9C%A8%E4%BB%B7%E5%80%BC" |

|

|

|

|

|

|

|

|

|

|

|

发表于 17-6-2008 08:02 PM

|

显示全部楼层

发表于 17-6-2008 08:02 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 17-6-2008 08:13 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 17-6-2008 08:18 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 17-6-2008 08:18 PM

|

显示全部楼层

回复 250# 财散人聚 的帖子

呢丢人同老散打斋打得多嘿毛?

皮嗨嗨又过来崖勒边打?

[ 本帖最后由 蚂蚁小弟 于 17-6-2008 08:23 PM 编辑 ] |

|

|

|

|

|

|

|

|

|

|

|

发表于 17-6-2008 08:23 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 17-6-2008 08:27 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 17-6-2008 08:30 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 17-6-2008 08:34 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 17-6-2008 08:39 PM

|

显示全部楼层

回复 257# 财散人聚 的帖子

|

呵呵,所以咪去冲下凉,食下野,打下机,睇下戏,沟下女,唱下歌甘咯 |

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 18-6-2008 01:42 AM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 18-6-2008 02:53 PM

|

显示全部楼层

有效资本市场假设理论

有效资本市场假设理论

虽然各种法学经济学理论嘈杂纷纭,对强制性信息披露制度的优劣莫衷一是,但任何一个研究现代证券法的人都无法忽视近二十年来得到各国证券法学界广泛承认的一个极为重要的金融经济学理论,即所谓“有效资本市场假设”理论(Efficient Capital Market Hypothesis-ECMH)

25.有效资本市场假设理论为围绕强制性信息披露制度展开的讨论提供了一个理论舞台。在这一理论出现之后,有关信息披露制度的各种论战,无论其依据的理论是源于法学、经济学还是社会学,都得以围绕着有效资本市场假设理论所建筑的构架和所提出的假设命题展开,从而进行实质意义上的真正交锋。而在此之前,各家各派常常争得面红耳赤,彼此的观点却往往擦肩而过,可言者,闻者昏昏。这一理论的最初鼓吹者费玛(Eugene Fama)认为,资本市场机制的运作效率在不同信息环境下有三种“有效”形式,即弱式有效、半强式有效和强式有效

26.进而言之,如果资本市场是有效的话,政府对信息披露的任何强制性要求都成为多余的。费玛以后,许多学者都用实证的和推理的方法试图从正面或反面来证明这一命题。迄今为止,有关这一理论的探讨并未就政府应当在证券市场效率方面起什么样的作用这一问题得出定论

27.但事实上,有效资本市场假设理论最重要的贡献并不在于它对应有什么样的证券管理体制和证券法规得出一个结论,而在于它作为一个描述性理论,表明了宏观、中观及上市公司层面的财务信息(包括任何影响金融指标的信息)的披露与证券价格之间的关系。这一理论建立了一个分析系统,让人们在该系统所设定的框架内,对股票价格本身的合理性,股票价格与信息披露和市场上其它各种因素的关系进行进一步的研究,从而得出自己的结论。过去二十多年来,经济、法律学界的许多学者对这一理论进行了深入、广泛的研究,写了大量的论著。虽然至今各学者的说法仍是见仁见智、了无定论,但所有对证券法学理论的严肃研究都不能不涉及这一理论。各国强制信息披露政策的制定以及对强制信息披露制度成功与否的评判也大多以此理论作为出发点。因此,我们有必要在此对这一理论进行更为深入的探讨。

(一)何为有效?

首先,什么样的市场是有效的市场?在一个有效的市场上,大量买主与卖主之间的相互行为形成一个特定商品的价格,这一价格应该能够全面反映有关该商品的所有公开信息。更重要的是,在出现任何新的信息时,上述价格应该能够立即作出反应。此处的关键在于“立即”二字,即由于价格能够极为迅速地对市场上新信息的出现作出反应,致使无人可以因为对信息的占有而获利。如果股票市场确实有效,则没有人可以因分析公开信息(无论是公司股票的历史价格走向还是公司的基本面数据)而获利。也就是说,在证券市场价格曲线的任一点上的价格均最真实、最准确地反映了该证券的价值

28.

有效市场有益于整个社会,因为价格真实地反映价值,致使资源在竞争中得到合理配置。但是,人们对任何一种特定证券的价值的认识并不相同,所以他们对何为“有效市场”的衡量标准亦无法相同。作为研究对象,我们可以暂时把这一标准定为“特定时段内对价值的最可能接近的衡量”。一般来说,这一价值应该处于对市场的极乐观的判断与极悲观的判断之间的某一点上。事实上人们对价值的认识的不确定性并不会过多地干扰市场有效性的存在,也不会干扰为保护市场的有效性而存在的一些基本条件,如信息披露和内幕交易方面的某些法规等。这一点本文将有进一步的阐述。

[ 本帖最后由 蚂蚁小弟 于 18-6-2008 03:10 PM 编辑 ] |

|

|

|

|

|

|

|

|

|

|

|

楼主 |

发表于 18-6-2008 02:54 PM

|

显示全部楼层

三种有效市场 信息性有效与价值性有效

(二)三种有效市场

如前所述,有效资本市场假设的基本理论将市场分为三种形式的有效市场,即弱式、半强式和强式有效市场

29.

1.弱式有效市场

在弱式有效市场存在的情况下,可以假定在这一市场上参加交易的所有投资者均掌握了某一特定证券的历史(自上市以来)价格变动情况及这些变动所反映的全部信息。也就是说,所有投资者占有的历史信息是一样的

30.所有投资者对这些信息的集体判断形成了这一特定证券的价格。由于这一价格所包含的是所有的历史信息,我们姑且称之为“昨天的价格”。但是,昨天的价格既不能用来说明今天的价格,也不能用来预测明天的价格。通过对证券价格的长期跟踪、分析,人们用“随机行走过程”(Random Walk Process)这一理论来形容某一特定股票的将来价格与其过去价格的关系。在随机行走过程中,股票连续的各次变动在统计链上是相互独立的,或者可以说,其序列相关系数为零。这就好象一群在空场上散步的人没有计划、没有目的地走来走去,使人完全没有办法预测其规律一样。过去的价格完全无法被用来预测将来的价格变化。研究股价历史完全无法给人带来赢利的机会。

2.半强式有效市场

在半强式有效市场存在的情况下,可以假定在这一市场上所有参加交易的投资者所占有的有关某一特定上市公司的所有公开信息都是一样的

31.这些信息一般即为投资公众对之明显感兴趣的信息,如关于公司业务损益的财务报告,分红、送配股的决定,会计调账,新闻媒介对公司的评价,直至中央银行政策的变动等等

32.证券价格反映了所有公开信息所包含的价值,也就是说,证券价格的形成反映了所有投资者对所有公开信息的集体判断。

3.强式有效市场

在强式有效市场存在的情况下,可以假定在这一市场上所有参加交易的投资者都掌握了有关某一特定上市公司的业绩及其内在价值的所有信息,无论其公开与否。也就是说,所有投资者,无论是否特权群体,所占有的信息都是一样的

33.证券价格反映了所有这些信息所包含的价值。

(三)信息性有效与价值性有效

有效资本市场理论在描述了三种形式的“有效市场”之后,进一步提出了一个从社会学和宏观经济学的角度看也许是更为重要的问题,即市场的“有效性”对于市场和社会究竟起到什么样的作用?换言之,即使是在已经证明了的“有效市场”上,人们仍然会进一步提出这样一个问题,即这里所说的“有效”用什么尺度来判断?通常我们所讲的信息作用于市场所发生的股价变动的速度只能被直观地称为“信息性有效”。而由于上述股价变动所造成的资本流向的改变,以及进而形成的整个社会资源的再分配则可被称之为“价值性有效”。

如上所述,对于信息性有效的市场上的股价是否准确真实地反映了其内在的价值,即一特定企业的基本面价值,这一点并无定论。而且对于研究一般市场行为及其获利机制的人来说,这一点似乎也并不重要。

另一个同样没有定论,但至少对政府决策者来说却是至为重要的问题是,信息性有效是否会导致价值性有效。如然,则肯定了许多人对证券市场所持的传统资本主义式的理解,即社会资源的再分配只须通过不受政府干预的资本市场的运作即可解决。以美国为代表的部分市场经济国家对证券市场所持的一般态度即是这种“自由放任主义”(Laissez Faire)的态度。但即使是在这样的制度下,我们也会不时地发现政府以调整社会资源为理由对市场作出事实上的干预

34.在其他许多国家里,政府对资本市场在更大程度上的干预态度则表现出对上述命题的否定性回答。中国目前的证券管理制度,无论是在发行审核过程中实行的所谓产业政策,在交易市场上对国有股、法人股给予的特殊“照顾”,还是公司、证券法规对国有企业的各种优惠政策,都充分表明了政府管理层和立法当局对证券市场的信息性有效能否导致价值性有效所持的怀疑甚至否定的态度。

[ 本帖最后由 蚂蚁小弟 于 18-6-2008 03:09 PM 编辑 ] |

|

|

|

|

|

|

|

|

|

| |

本周最热论坛帖子 本周最热论坛帖子

|

(1)

(1)

(2)

(2)

(3)

(3)

(3)

(3)  (4)

(4)  (5)

(5)  (6)

(6)

(7)

(7)

2991

2991  90

90