|

|

【MELEWAR 3778 交流专区】美丽华工业

[复制链接]

[复制链接]

|

|

|

发表于 16-7-2007 11:22 AM

|

显示全部楼层

发表于 16-7-2007 11:22 AM

|

显示全部楼层

原帖由 mjchua 于 16-7-2007 10:21 AM 发表

起到 RM1.80 了 以價值投資法 是不是不止這個價錢 ?

已经上车了也等了好一段时间

目前这个价位我还不是很满意咯 |

|

|

|

|

|

|

|

|

|

|

|

发表于 16-7-2007 12:06 PM

|

显示全部楼层

|

|

|

|

|

|

|

|

|

|

|

发表于 16-7-2007 02:49 PM

|

显示全部楼层

原帖由 mjchua 于 14-7-2007 05:37 PM 发表

| 上市子公司 | 目前股價 | 匯率 | 股票總數 | 股權 | 市值 | | m3nergy | 1.540 | 1.000 | 125,064,172 | 22.60% | 43,527,334.42

| | mycron | 0.965 | 1.000 | 179,000,000 | 54.50% | 94,140,575.00 | | Gindalbie | 1.420 | 2.990 | 430,989,000 | 17.19% | 314,558,623.24

| 子公司總市值

|

|

|

|

| 452,226,532.66

| | 總資產 |

|

|

|

| 978,742,000.00 | | 總債務 |

|

|

|

| -355,311,000.00 | 淨資產

|

|

|

|

| 1,075,657,532.66

| | MIG 股票總數 |

|

|

|

| 226,227,011 | | 每股淨值 |

|

|

|

| 4.75

|

原帖由 mjchua 于 14-7-2007 06:10 PM 发表

我不知道有沒有算錯 有哪位前輩可以幫忙 double check 一下

有一項可能要扣出來 Investment in associates 94.3m (若這 investment 有包括上市公司)

原帖由 mjchua 于 14-7-2007 08:29 PM 发表

誰可以幫忙查一查 看我的算法有沒有問題呢 ?

请问mjchua兄的总资产RM978,742,000.00是如何得到的?总资产有没有包括子公司的资产?

2006年报内的note 11, 12和15,你有留意吗? |

|

|

|

|

|

|

|

|

|

|

|

发表于 16-7-2007 02:51 PM

|

显示全部楼层

原帖由 Mr.Business 于 16-7-2007 02:49 PM 发表

请问mjchua兄的总资产RM978,742,000.00是如何得到的?总资产有没有包括子公司的资产?

2006年报内的note 11, 12和15,你有留意吗?

我有看 note 11 和 note 12 |

|

|

|

|

|

|

|

|

|

|

|

发表于 16-7-2007 02:57 PM

|

显示全部楼层

原帖由 Mr.Business 于 16-7-2007 02:49 PM 发表

请问mjchua兄的总资产RM978,742,000.00是如何得到的?总资产有没有包括子公司的资产?

2006年报内的note 11, 12和15,你有留意吗?

看 #74 和 #76 是 note 11 和 note 12

note 15 之前沒有看到 現在正在看 |

|

|

|

|

|

|

|

|

|

|

|

发表于 16-7-2007 03:09 PM

|

显示全部楼层

回复 #83 Mr.Business 的帖子

我研究Melewar的最新季度报告 (31/03/2007),里面的Assets是有考虑在子公司和Associate company的投资的,所以我觉得:Total equity= RM623.431M;而MIG的票数是226,227,011股,因此每股净资产是RM2.75。

[ 本帖最后由 Mr.Business 于 17-7-2007 02:03 PM 编辑 ] |

|

|

|

|

|

|

|

|

|

|

|

发表于 16-7-2007 03:14 PM

|

显示全部楼层

原帖由 Mr.Business 于 16-7-2007 03:09 PM 发表

我研究Melewar的最新季度报告 (31/03/2007),里面的Assets是有考虑在子公司和Associate company的投资的,所以我觉得:Total equity= RM623.431K;而MIG的票数是226,227,011股,因此每股净资产是RM2.75。

那你知道在 31/03/07 的時候 他們估算其他 financial gain 是多少嗎 ? Gindalbie 的價值是多少嗎 ? |

|

|

|

|

|

|

|

|

|

|

|

发表于 16-7-2007 03:19 PM

|

显示全部楼层

原帖由 Mr.Business 于 16-7-2007 03:09 PM 发表

我研究Melewar的最新季度报告 (31/03/2007),里面的Assets是有考虑在子公司和Associate company的投资的,所以我觉得:Total equity= RM623.431K;而MIG的票数是226,227,011股,因此每股净资产是RM2.75。

我覺得扣去 2006 年的 :-

note11 investment in associates 86,199,131

note12 subsidiary companies 42,000,000

note15 other financial gain 85,098,473

Total : 213,297,604

所以調整後 RM4.75 - RM0.94 = RM3.81 |

|

|

|

|

|

|

|

|

|

|

|

发表于 16-7-2007 03:22 PM

|

显示全部楼层

原帖由 mjchua 于 16-7-2007 03:19 PM 发表

我覺得扣去 2006 年的 :-

note11 investment in associates 86,199,131

note12 subsidiary companies 42,000,000

note15 other financial gain 85,098,473

Total : 213,297,604

所以調整後 RM4.75 ...

TA Securites 估算的是 NAV 是 RM3.39 (有些 items 經過 15% discount)

謝謝 Mr. Business 指出這個 |

|

|

|

|

|

|

|

|

|

|

|

发表于 16-7-2007 03:27 PM

|

显示全部楼层

原帖由 mjchua 于 16-7-2007 03:14 PM 发表

那你知道在 31/03/07 的時候

Gindalbie 的價值是多少嗎 ?

是这个吗?

|

|

|

|

|

|

|

|

|

|

|

|

发表于 16-7-2007 03:29 PM

|

显示全部楼层

回复 #89 mjchua 的帖子

mjchua兄,

不用客气。哈, 纯粹讨论而已.

其实股价起了,赚钱了,那才是最重要的。哈。 |

|

|

|

|

|

|

|

|

|

|

|

发表于 16-7-2007 03:36 PM

|

显示全部楼层

原帖由 Mr.Business 于 16-7-2007 03:27 PM 发表

是这个吗?

這個沒有細項 不知道有包含什麼

而且 3/31/07 gindalbie 還不到 0.8 現在是 上星期是 1.42 差了 aud0.62 |

|

|

|

|

|

|

|

|

|

|

|

发表于 16-7-2007 03:54 PM

|

显示全部楼层

回复 #92 mjchua 的帖子

Iron Ore Mining Operations (Gindalbie Metals Ltd)

The Group made an initial investment in an Iron Ore exploration and mining company named Gindalbie Metals Ltd (GBG) in 2004, by way of subscription via private placement, of 27.0 million shares, for a consideration of AUD 3.38 million. This represented an interest of 12.84% in the issued capital of thecompany.

During the year, through a rights issue exercise undertaken by GBG, the Group increased its shareholding further to 23.5% by subscribing for an additional 47.0 million shares, at a cost of AUD 4.24 million.

To fund their exploration and feasibility studies, GBG subsequently undertook several issuances of shares, by way of private placements. These fund raising exercises diluted our shareholding down to our current interest of 17.2%, consisting of a total of 74,087,009 shares at an average cost of AUD 0.10 per share.

Based on the market price of AUD 0.69 per share, as at 28 April 2006, this investment translates into an unrealised capital gain, of AUD 43.7 million (or RM 118 million) for the Group.

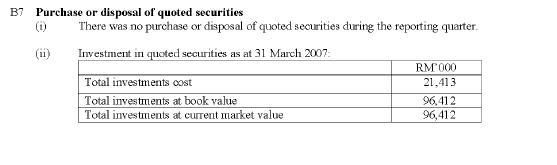

Melewar投资Gindalbie 的成本是AUD7408700.9 (74,087,009 x AUD0.10)。按照1AUD兑换RM2.89的汇率来计算,投资成本刚刚好是RM21411K。 |

|

|

|

|

|

|

|

|

|

|

|

发表于 16-7-2007 04:06 PM

|

显示全部楼层

原帖由 mjchua 于 15-7-2007 12:19 PM 发表

Table 4: Melewar's Sum-of-Parts

| FY08 Net profit (RMm)

| 12-Month PER (x)

| Value | | Steel | 32.8 | 14.0 | 459.4 | | Construction | 6.1 | 10.0 | 61.4 | | Associate - Gindalbie (NPV - 15% discount rate) | 265.2 | 0.0 | 265.2 | | Associate - M3Nergy | 1.5 | 14.0 | 21.0 | | Power - (NPV - 15% discount rate) | 135.6 |

| 135.6 |

|

|

| 942.7 | | Net asset value (RM'm) |

|

| 942.7 | | Borrowings (Company level) |

|

| (174.0) | | Share cap (m shares) - Fully diluted |

|

| 227.0 | | NAV per share (RM) |

|

| 3.39 | | 20% Discount |

|

| 0.69 | | Target Price |

|

| 2.70 |

|

|

| implied PER 10.5 |

原帖由 mjchua 于 15-7-2007 04:19 PM 发表

TA 的計算方法沒有把 MYCRON 計算進去

而且 TA 的計算錯了 把 M3nergy 的價值算少了很多

另外也把 Gindalbie 的市值打個 15% discount (而且是用 aud1.20 來計算, 現在是 aud1.42)

TA的分析员在评估Melewar的内在价值 (RM2.70)时是不考虑上市子公司的市价的,而是注重所有子公司的盈利能力。他预计钢铁部分在FY08的Net profit是RM32.8million,这Net profit应已经考虑MYCRON的盈利了。另外Gindalbie的RM265.2million不是指市值,而是指Gindalbie的盈利能力。你再研究看看就能明白他的计算了。

TA的Target Price (RM 2.70)刚好和我计算的每股净资产 (RM2.75)差不多。

原帖由 Mr.Business 于 16-7-2007 03:09 PM 发表

我研究Melewar的最新季度报告 (31/03/2007),里面的Assets是有考虑在子公司和Associatecompany的投资的,所以我觉得:Total equity=RM623.431M;而MIG的票数是226,227,011股,因此每股净资产是RM2.75。

[ 本帖最后由 Mr.Business 于 17-7-2007 02:03 PM 编辑 ] |

|

|

|

|

|

|

|

|

|

|

|

发表于 16-7-2007 04:08 PM

|

显示全部楼层

原帖由 Mr.Business 于 16-7-2007 03:54 PM 发表

Iron Ore Mining Operations (Gindalbie Metals Ltd)

The Group made an initial investment in an Iron Ore exploration and mining company named Gindalbie Metals Ltd (GBG) in 2004, by way of subscript ...

這段你是在 2006 年 annual report 裡找到的 ? 我試過 search "Gindalbie" 找不到 |

|

|

|

|

|

|

|

|

|

|

|

发表于 16-7-2007 04:11 PM

|

显示全部楼层

回复 #95 mjchua 的帖子

秘密。。。。。哈。

。

。

。

。

。

。

第九页。

MELEWAR-AGMNotice-ChairmanStat-CorpInfo(734KB) |

|

|

|

|

|

|

|

|

|

|

|

发表于 16-7-2007 04:15 PM

|

显示全部楼层

原帖由 Mr.Business 于 16-7-2007 04:06 PM 发表

TA的分析员在评估Melewar的内在价值 (RM2.70)时是不考虑上市子公司的市价的,而是注重所有子公司的盈利能力。他预计钢铁部分在FY08的Net profit是RM32.8million,这Net profit应已经考虑MYCRON的盈利 ...

你再看清楚一點 265.2m 是 value 不是 profit

Table 4 有三個 items, FY08 profit 和 Value 是不同的 |

|

|

|

|

|

|

|

|

|

|

|

发表于 16-7-2007 04:18 PM

|

显示全部楼层

原帖由 Mr.Business 于 16-7-2007 04:06 PM 发表

TA的分析员在评估Melewar的内在价值 (RM2.70)时是不考虑上市子公司的市价的,而是注重所有子公司的盈利能力。他预计钢铁部分在FY08的Net profit是RM32.8million,这Net profit应已经考虑MYCRON的盈利 ...

而且 M3Nergy 不只值那麼少 Power 和 Gindalbie 都打了 15% discount

算出來的 NAV RM3.39 再打個 20% discount 才會變成 RM2.70

TA Securities 的算法是非常保守

[ 本帖最后由 mjchua 于 16-7-2007 04:19 PM 编辑 ] |

|

|

|

|

|

|

|

|

|

|

|

发表于 16-7-2007 04:19 PM

|

显示全部楼层

原帖由 mjchua 于 15-7-2007 11:55 AM 发表

TA 分析報告 - 續二

Iron and Steel Division

......

Importantly, the group has made a bold move in investing upstream activities in buying into a mining company listed in Australian Stock Exchange named Gindalbie Metals Ltd. The group purchased Gindalbie back in May 2004 for AU$0.10 and now the price has reached more than AU$1.20. Based on the announcement by Gindalbie to Australian StockExchange on Friday (6 July 2007), the group has report an increase in Karara Megnetite resource to 1.43bn tones grading 36.3 Fe as compared to reserve of 1.29bn announced previously. Based on few reports we read on Australian Iron Ore sector, Midwest Australia where currently Gindalbie's Karara mines are located is becoming an important iron ore region in Australia, with potential similar to the established Pilbara Region. On the back of the envelope calculation, based on simple assumptions of

1)250mn tonne of magnetite over 40 years,

2) Magnetite price of US$55 per tonne,

3) Cost of recovery of USD30/tonne,

4) Capex and Financing 15% of total GPV and

5)discount rate of 15%, we arrived at Net Present Value of RM265mn or RM1.17 per share (Appendix 1).

On the other hand, if we take the last closing price of AU$1.20 for Gindalbie, the group should be worth RM266mn or RM1.17 per share. It is important to highlight that our net present value assumptions are very conservative given that the total Magnetite sold throughout the periodis only 250mn tonne as compared to the reserve of 1.43bn tonne.

原帖由 mjchua 于 15-7-2007 12:31 PM 发表

Appendix 1: Gindalbie's Assumptions & Valuation

Potential 1.43 bn tonne

|

| Scenario

|

| | Recovery (mn tonne) | 250

| 500 | 750 | | Avg Magnetite (USD/tonne) | 55 | 55 | 55 | | Gross production value (USDmn) | 13,750 | 27,500 | 41,250 | | Cost recovery: |

|

|

| | Operating @ USD30 | 7,500 | 15,000 | 22,500 | | Capex and Financing @ 15% of GPV (USDmn) | 2,063 | 4,125 | 6,188 | | Pretax | 4,188 | 8,375 | 12,563 | | Tax @ 35% (USDmn) | 1,466 | 2,931 | 4,397 | | Net Attributable to Gindalbie after tax (USDmn) | 2,722 | 5,444 | 8,166 | | Melewar’s portion @ 17% (USDmn) | 463 | 925 | 1,388 | | Initial Investment Outlay (USDmn) | 6 | 6 | 6 | | Enhancement (USDmn) | 456 | 919 | 1,382 | | NAV @ RM3.50 per USD 1 (RMmn) | 1,597 | 3,217 | 4,836 | | NPV 15%, 40 years | 265 | 524 | 788 | | NAV per share | 1.17 | 2.31 | 3.47 |

请问各位网友,这 "discount rate of 15%, we arrived at Net Present Value of RM265mn or RM1.17 per share",是用什么方程试计算出来的?可以清楚列出来吗?

[ 本帖最后由 Mr.Business 于 16-7-2007 04:21 PM 编辑 ] |

|

|

|

|

|

|

|

|

|

|

|

发表于 16-7-2007 04:23 PM

|

显示全部楼层

原帖由 mjchua 于 15-7-2007 11:59 AM 发表

TA 分析報告 - 續三

Power and Oil & Gas divisions - Diversification Strategy

The group continues to diversify its income stream investing in thenext in-thing, which are the power and oil & gas industries. Thegroup holds 70% stake in Siam Power Generation Compnay Ltd which holdsa total licensed capacity of 450MW to built, operate and own powerplant in Rayong, Thailand. The group would construct the 1st phase185MW which is expected to start operation in 2009 and has signed thePPA with EGAT for 25 years, with fuel pass through and index to the UScurrency. Based on the current fuel price and currency, the averageselling price is around US$0.0753/kwh which translates to RM0.26/kwh.Although non-committal, we believe the IRR of the project is above15%,similar to the first generation PPA signed in Malaysia. Just toillustrate the value of such IPP to investor, we have made a roughcalculation to find the value of the power division. Based on a flatUS$0.0753/kwh and 180MW capacity for the next 22 years at 90% capacity,the power division would enhance the group's NAV by RM136mn (based ondiscount rate of 15%) or RM0.60 sen per share (Appendix 2).

原帖由 mjchua 于 15-7-2007 12:36 PM 发表

Appendix 2: SEPCO's Assumptions and Valuation

Potential 450 MW

| Installed Capacity (MW) | 180 | 360 | | Capacity Utilisation (%) | 90 | 90 | | Capacity Utilisation (mn kw/h) | 1,380 | 2,760 |

| 0.0753 | 0.0753 | | Revenue (USDmn) | 104 | 208 | | EBIT Margin: |

|

| | 30% | 31 | 62 | | Capex and Financing @ 15% of GPV (USDmn) | 16 | 31 | | Pretax | 16 | 31 | | Tax @ 35% (USDmn) | 5 | 11 | | Net Attributable to SEPCO after tax (USDmn) | 10 | 20 | | Melewar's portion @ 70% (USDmn) | 7 | 14 | | Initial Investment Outlay (USDmn) | 1 | 1 | | Enhancement (USDmn) | 6 | 13 | | NAV @ RM3.50 per USD 1 (RMmn) | 21 | 46 | | NPV 15%, 22 years | 136 | 293 | | NAV per share | 0.6 | 1.29 |

请问各位网友,这 "discount rate of 15%, we arrived at Net Present Value of RM136mn or RM0.6 per share",是用什么方程试计算出来的?可以清楚列出来吗? |

|

|

|

|

|

|

|

|

|

| |

本周最热论坛帖子

|

2927

2927  51

51